I have two offers from startups. How do I choose which one to pick?

A lot of the answers given basically boiled down to:

- Go with your gut (who do you believe in, which founder/team did you like, whose vision gets you excited?)

- Try to evaluate them like a VC would

Both of those answers are inadequate to terrible because (1) going with your gut isn’t a great way to make a decision about your career and (2) trying to play armchair VC is pretty tough. Heck, the data shows that most VCs aren’t great pickers of startups themselves, and they get paid to do this.

So what are some tests using data or some simple heuristics a candidate could use to make a big decision in a more informed, evidence-based way when faced with multiple job offers from startups.

First, a few notes about the tests and who and how you should use them:

- These tests use data. They don’t consider squishy stuff. The tests aim to be black & white. I’m assuming you like the company, the founders and team you’ve met and think you could work there. I’m assuming the compensation and equity are comparable. In some sense, these tests might convince you against a startup who you like. They don’t consider the charisma of the CEO or how nice the office is or the free beer they might have on tap. If those are important decisions in your evaluation, keep those in mind. These tests don’t consider those factors. (note: don’t prioritize beer)

- These work primarily for tech companies. The tests have applications across all types of startups but might be slightly more appropriate for tech startups.

- Uber is not a startup. If your offers are from Uber and Airbnb, these tests probably won’t help you. If you’d like to believe those companies are startups because you’d like to say you work in tech at a startup, you’re welcome to delude yourself. But when you’re worth $25B (Airbnb) or $65B (Uber), a startup you are not. In other words, these tests are probably best for early- to mid-stage startups and not for later-stage unicorns. They also won’t be good for concept stage startups where it’s 2 friends in an apartment and you’re going to be the first hire. Related good read: Hunter Walk of VC firm Homebrew details why mid-stage startups are the best bet for new grads which may be useful.

- You care about upside. I’m assuming that you care about the professional and potential financial upside of joining a winner and are willing to work somewhere for 3-4 years to deserve that upside. The financial upside will come from either equity or salary/bonus that comes over time. If you just want to be part of the startup scene, these tests may not be good for you. In other words, these tests assume that you prefer employment to unemployment and more money to less money. They also implicitly assume that if you join the right startup, you’ll do the work to get the upside. As Charlie Munger has said “To get what you want, deserve what you want. Trust, success and admiration are earned.” Alright, this is getting a bit philosophical so let’s get back to the data.

- A startup need not score well on every test – You want to evaluate them against these 9 tests, but you may not have enough data to assess each one. You want a startup that does well on many of these tests.

- Applies to VC-backed companies – not RABBITS. These tests apply to VC-backed startups. If you’re thinking of joining an unsexy, revenue-funded (aka bootstrapped) company that makes more money than it spends every month, these tests may not all apply. In other words, these tests may not apply to RABBITs (Real Actual Businesses Building Interesting Technology). BTW, RABBITs are underrated so if you find one, think about it.

So if you’re still reading after those caveats, let’s get to the data and the tests.

Some of the tests are easier with access to CB Insights but you can do all of them with a bit of research on your own. University career offices and their students with access to CB Insights can do all of these online in a few clicks.

Test 1 – Do they have enough money in the bank?

Companies generally raise every 18 to 24 months. So if they raised nearly 18 months ago, be cautious.

“But the CEO said they’re close to finalizing their round”

That’s great. Almost closing their round and having closed their round are two very different things especially in the current financing market. There are never any guarantees.

If they raised more than 18 months ago, you’re taking a bit more of a risk so ask more questions. Ask them about their financing plans and current cash position of the business. They probably won’t give you the exact figures (I wouldn’t), but it’s a fair question and you should get a sense for how solid they are by the quality of the answer you get.

It’s conceivable they’re a SaaS (software-as-a-service) business who is making money and so doesn’t need to raise immediately due to cash coming in but you should understand this. See the market opportunity section below on how to understand this better.

But the ability to raise the next round is important for VC-backed companies. The startup VC funnel is a brutal one as the graphic below illustrates. So again, unless the round is closed — it ain’t closed. Promises of investors who are on the verge are just that — promises.

Test 2 – Are the investors / VCs any good?

When a company says they are “venture-backed,” the truth is that it doesn’t really mean much, because it depends on who your investors are.

And so when evaluating as startup that says they are VC-backed, you need to look at the investors. Have they invested in winners in the past? Is the company backed by the best VCs or just another VC? There are tons of folks with some money from family offices and a $15 million fund who call themselves VCs. There is a world of difference between them and really good VCs.

Here is a plot of the exits over time of Sequoia Capital. Look at the number of recent exits over $1B and $10B. Good sign. A list of funds who are top tier are below.

Below is graph of a “popular” fund (popularity as determined by their blog posts and Twitter activity). I’ve not included their name for obvious reasons but just to illustrate that VC-backed means very different things.

If deciding between 2 startups and one is backed by investors with a recent and solid track record and one is backed by investors who don’t have a track record, performance wins. Of course, one key thing here is recent track record. If their best investments were in 1999, that doesn’t count either.

Here is a power ranking in which VCs rate their fellow VCs. If the VC investor in the company is on this list, that’s a good thing.

One caveat — if the well-known firm invested at the seed stage and didn’t follow-on in the Series A, it might be worth a deeper look to understand why. Signaling risk is what they call it.

If they raised from a micro-VC fund (a smaller VC) that cannot follow-on in every round, you want to see if they’re good at getting their companies follow-on financing.

Test 3 – Who is the venture capitalist on the company’s board?

Also, look at who is on the board from the VC. Are they on this list of the top 100 individual VC partners we did in partnership with The New York Times? Again, if these folks are on the board, that’s a good thing. If it’s a junior partner from a well known firm or a principal, that’s not a bad thing unto itself, but it’s worth digging.

In addition, look if the VC lists the board relationship on their LinkedIn, Twitter and/or on their website. If they list others and don’t list the startup you are evaluating, that may actually be a bad sign. Venture capitalists often don’t want the stench of a bad startup on them so they’ll distance themselves from dogs where feasible. There is nothing wrong with this either. Folks want to be affiliated with winners – not losers, and it is only natural.

Test 4 – Is the market they’re targeting big enough?

This is hard but is a critical thing to understand. If the startup is targeting a total addressable market worth $100 million, even great execution (they capture 20% of the market) means that the startup will only be a $20 million revenue business.

The word “only” might throw you there but in the VC-backed tech company biz, it’s go big or go home. $20 million revenue is rarely big enough to provide a meaningful exit for a VC-backed company. And as Steve Blank says “when you take VC, their business model becomes yours.” In other words, your startup, if VC-backed, needs to be aiming big.

To understand market size, Christoph Janz at Point Nine Capital has a pretty simple and effective framework that is worth evaluating your startup offers against. It looks at five ways to build a $100 million business. So when looking at the the startup’s market, you look at the number of customers in the market and the ARPA (average revenue per account).

Christoph writes:

To build a Web company with $100 million in annual revenues*, you essentially need:

- 1,000 enterprise customers paying you $100k+ per year each; or

- 10,000 medium-sized companies paying you $10k+ per year each; or

- 100,000 small businesses paying you $1k+ per year each; or

- 1 million consumers or “prosumers” paying you $100+ per year each (or, in the case of eCommerce businesses, 1M customers generating $100+ in contribution margin** per year each); or

- 10 million active consumers who you monetize at $10+ per year each by selling ads

So when evaluating your startup, if their product is $100/year, you have to assess whether they have the potential to have 1 million paying accounts. In order to get 1 million people paying, there probably needs to be 100 million potential accounts, i.e. a back of the envelope assumption that you’ll get a 1% conversion of the total market.

It’s worth figuring out if they have a legitimate shot of getting to the $100 million revenue number and the above framework is a good way to do that. Related: Boris Wertz of VC firm VersionOne also has a good post on building a $100 million business.

Test 5 – Has the startup’s market/industry had any successful outcomes?

This test is best applied to startups that are entering a defined or semi-defined market which is most of the time. Here you want to look for industries or markets that have had successful exits, either by virtue of public offerings (IPOs) or large M&A. Are their well-heeled acquirers buying companies in the market?

Of course, this test may not work on very new or very hot emerging markets. But in more established markets/industries, it can work.

For example, HR tech (or human capital management tech or HR & workforce management tech) is an industry with many acquisitions and some very large exits via IPO and M&A as you can see below. There are numerous IPOs (orange) and the M&A activity has also stepped up over time (blue bar). You can quickly analyze 500+ sectors/industries like this with Industry Analytics.

On the flipside, if we look at the news aggregation / news reader space, there have been lots of casualties. Sure, one may break out, but historically, it’s been a place where good money goes to die.

Test 6 – Is the market the company plays in still hot?

Sentiment about an industry is important especially when you might be joining a venture-backed company that is burning money (burning money, burn, or burnrate occurs when expenses exceed revenues). When a company is burning money, it will likely need to raise additional capital from investors.

And so sentiment about an industry in which a company competes is important as it plays a role in raising money. Yes, unfortunately, there is a herd mentality among investors.

So if you just got an offer at an amazing daily deals company or flash sales company or a mobile gaming company, you might want to scrutinize it just a bit more.

Startups are hard enough to execute on. When the market is working against you, it’s even harder.

For university career services who have access to CB Insights, a quick way to see how much buzz there is about an industry is by using CB Insights Trends. Here are a couple that are not trending well in terms of buzz, i.e. quantified self and daily deals.

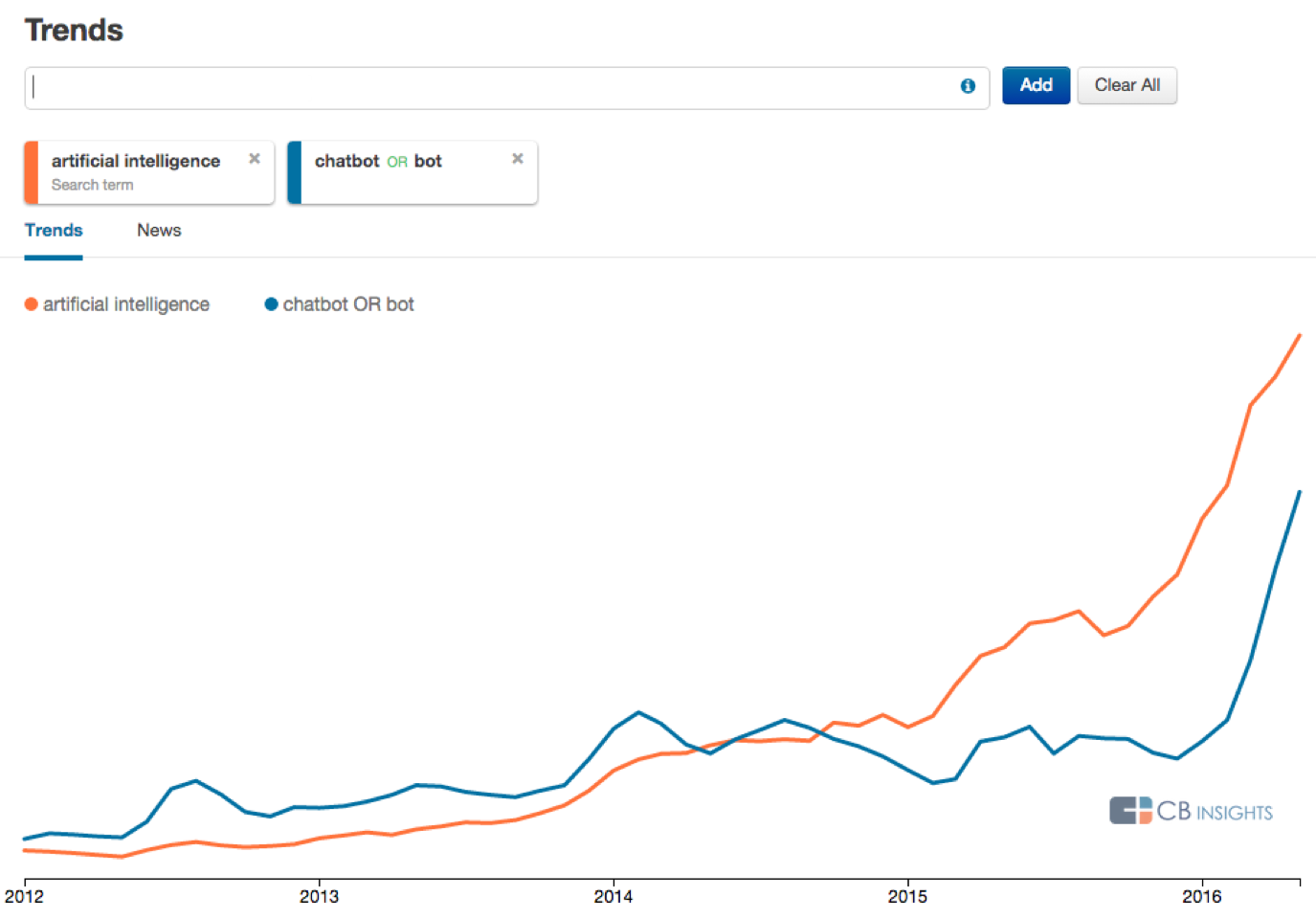

And here are some where buzz continues to gain steam: artificial intelligence, chatbots, internet of things, and the industrial internet of things.

Test 7 – Are the non-financial metrics like hiring, web traffic, news mentions trending up or down?

Because these are private startups, financial results are difficult to come by outside of financing or valuation data you’d find on CB Insights. And unless you are very senior, you probably won’t have enough leverage to get access to any financial data in making your decision.

But you can use a variety of non-financial performance metrics to get a sense for if things are going well.

For example, has the company’s hiring velocity been steady or accelerating or declining?

Are they hiring in business development or sales which might indicate they’ve gotten product/market fit and are scaling up? Or did they just hire a CFO or head of HR or in-house recruiters which might also indicate growth?

You can do this manually by looking at their jobs page or visiting job search engines. If you’re a university student with access to CB Insights, you can search for startups that are hiring on deal or company search as well and by viewing the hiring trend on a company’s profile.

startup job hiring

startup job hiring

Other signals to look for are things like:

- Is website traffic growing?

- How about social media chatter?

- What about news mentions?

On CB Insights, view these on the Performance Metrics tab or via search.

You can track news chatter about a company using Trends, and media chatter can be quite illuminating.

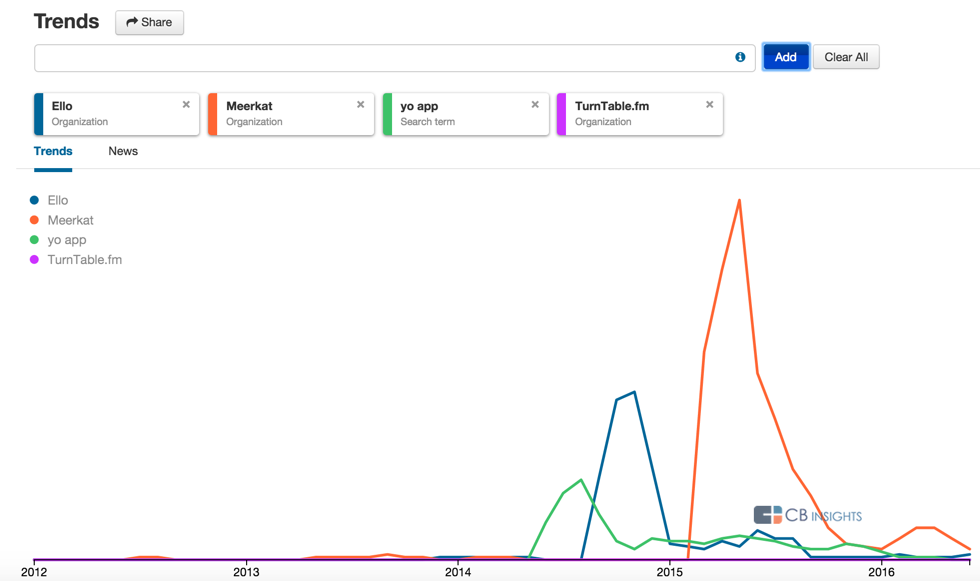

For example, for consumer tech companies (B2C), are they getting more buzz? Or did they get a lot of buzz and then fizzle out? It’s tough for consumer oriented companies to come back after getting their initial shot. Not impossible — but def rare. Here’s the Trends graph for some recent buzzed about consumer-tech companies like Ello, Meerkat, Yo! and Turntable.fm. They all had their initial bounce and popularity but declined quickly after that.

Note: you can modify this Trends search on CB Insights. Just click the link.

Does the startup you are looking at have a big spike and then nothing or a steady uptick in media mentions?

Although media might be more useful for consumer tech companies, it can still be a useful measure for B2B (business-to-business) companies. Here’s the Trends chart for yours truly, CB Insights. While a B2B tech market intelligence platform like us won’t get the level of coverage of Snapchat, looking at the trend and observing whether it’s gaining traction or not is still useful as a proxy for the company’s traction.

Test 8 – Are they outfunded by a competitor?

If the startup you are evaluating is outfunded by a competitor, it’s worth looking at how those competitors fare on the tests above. Money doesn’t buy the ability to execute so just because a company is outfunded doesn’t mean it’s not worth joining.

But if they’re outfunded and the competitors do better on the tests above, it’s worth asking if they have a real shot at winning?

To compare level of funding, you can visit a company’s profile and will see a company relative to comparable companies as can be seen below.

Test 9 – Is employee turnover too high? And at what levels?

This is a new test which we love.

Use the amazing Wayback Machine (Internet Archive) to look at the company’s website from an earlier period with a focus on their team page (if they have one) and see how many folks from that page are still working at the company. A lot of turnover here should prompt a why.

Also, look at LinkedIn and use the advanced search to look for former employees. If the ratio of former employees to current employees is high, that’s another red flag. While some past employees on LinkedIn and is fine and probably healthy, if you have 45 employees today and 45 former employees, that might indicate a problem.

Hope this proves useful. None of these tests individually are the key to making a good decision but taken together with your gut and qualitative insights you’ve gathered, they should help steer you in the right direction.

All the data, visualizations and trends above came from CB Insights.

Good luck.

header image from here