The following is a guest post co-authored by Samir Kaji (@samirkaji), managing director at First Republic Bank (@firstrepublic) and Jessica Peltz-Zatulove (@jessicapeltz), principal at kbs+ Ventures (@kbspvc)

The past few years have seen Corporate Venture Capitalists (CVCs) play a larger role in the private markets

CVCs participated in deals that deployed over $12B into startups in 2014, according to CB Insights, a number that is expected to be matched or exceeded in 2015. Notably, CVCs participated in financing totaling nearly $3B across 240 deals in Q3’15. This investment represented 14.1% of total venture dollars funded during the quarter. One-fifth of all venture deals in Q3’15 included CVC participation. Along with the increase in funding has come an influx of new firms. Since 2014, over 127 new CVCs have been formed, further validating CVCs as viable and valuable sources of capital within the startup ecosystem.

Given that backdrop, it’s important for operators to understand the distinction between CVCs and traditional venture capital (VC) firms. In contrast to traditional VCs, which invest third-party capital with the sole objective of financial return, CVCs may have several objectives unrelated to financial return. As a result, CVCs often have different approval processes, value propositions, and funding structures.

In an effort to share some common themes within the CVC world, we surveyed a subset (n=34) of CB Insights’ most active CVCs to better understand the current landscape.

1. Objectives and Motivations of CVCs

In an effort to innovate at a pace afforded by nimble startups, CVCs often invest for primarily strategic reasons, with financial return being a secondary item on the decision tree. The vast majority of CVCs in our survey (4 out 5) named strategic value as key decision driver, but nearly the same proportion listed financial return as being equally important. This may sound intuitive, but it is significantly different from the messaging of early CVC arms. Additionally, firms such as Sapphire Ventures (formerly SAP Ventures) have publicly stated their primary motivation is financially driven.

While vetting CVCs, it’s important for entrepreneurs to fully research a prospective CVC investor to ensure proper investor-company alignment. This should include understanding the unique pain points of the CVCs affiliate organization and determining whether your technology solution is symbiotic with their organization.

2. Source of Capital

While traditional Venture Capital firms raise capital from third-party Limited Partners such as endowments, pension funds, Fund of Funds, and family offices, CVCs are typically funded solely through their company’s balance sheet. In our survey, 76% of CVCs leveraged only balance sheet cash, often through a legally independent corporate fund. Only 9% of funds we talked to included personal capital from the company’s senior leadership. This is important for entrepreneurs to understand, primarily because micro-economic conditions specific to that company have the potential to impact follow-on financings or timing of an investment close. For example a CVC partner may request funding an investment in January (or the start of a new fiscal year) vs. December based on broader organizational mandates.

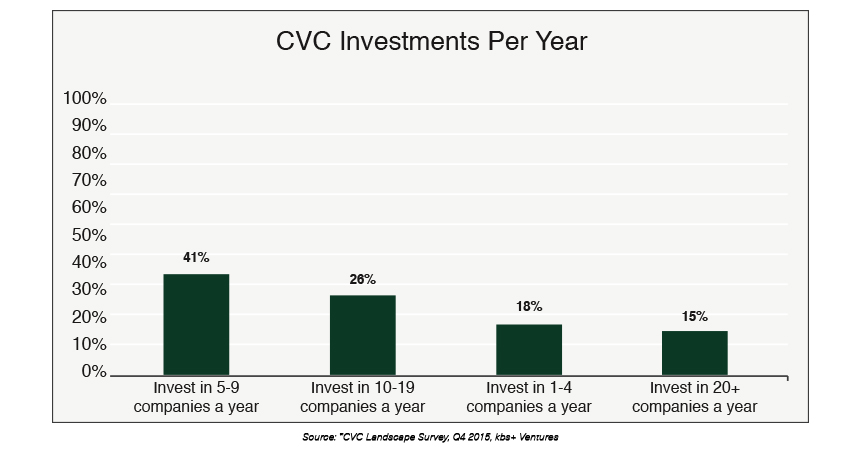

3. Dedicated Funds vs. Opportunistic Capital

67% of CVCs have a dedicated venture budget of capital to deploy over a designated timeframe, while 29% of our survey respondents employ an “opportunistic” approach – making investments opportunistically throughout the year. Since the number of deals done each year varies greatly across CVCs, founders should inquire about how many investments the CVC has closed within the prior year to better understand the institutional commitment the firm has toward startup investment and support. The CVCs that do 10+ investments per year typically have dedicated teams and budgets to deploy to startups.

Note the chart below does not include follow on investments.

4. Approval Process and Timeline

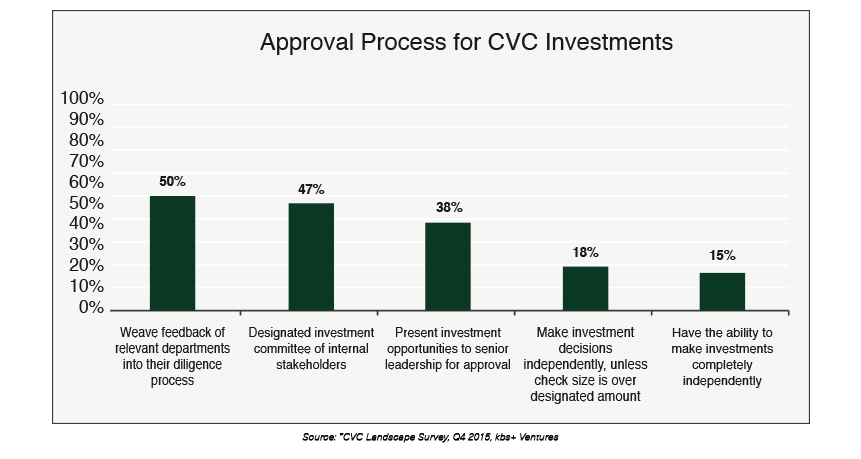

In contrast to traditional VC firms, partners at CVCs often cannot make investment decisions independently (there are of course some exceptions); senior leadership, business units, and various internal stakeholders of the affiliate company contribute to both the diligence process and final approval. 50% of CVCs weave the expertise and feedback of relevant departments into their due diligence process – while this improves the probability for the CVC to get buy-in for post-investment internal collaboration, it can also result in a deal not getting done because of a real or perceived lack of synergies within the CVC’s organization.

Of course the more complex the approval process, the longer the time from initial meeting to funding, an important consideration for entrepreneurs that are contemplating CVC capital. To adapt, CVCs have been accelerating the approval timeline to help ensure participation in time sensitive rounds. 59% of CVCs work to get approval (from the first meeting) within 2 months, while 32% project a 2-4 month turnaround, and ~9% estimate more than 4 months to come to a decision. Of course, this is also subject to size of investment and stage of company.

5. Post-Investment Support

While many companies have historically posited that CVCs placed too much emphasis on their own organizational objectives, the vast majority of CVCs today actively provide their portfolio companies with transparent domain expertise and a direct tie-in to a vast network of value-add relationships. 56% of CVCs consider their team very involved in helping to build their portfolio companies, 35% of CVCs mentioned that they provide ongoing support as needed, while only 3% noted they offer very little assistance to their portfolio companies. Consistently, we were told CVCs strive to provide their portfolio companies with access to potential reference customers, domain expertise, and connections to strategic partners.

When taking capital from CVCs, it’s critical for founders to investigate how that CVC can help with the scaling of their business. Founders should also do due diligence through reference checks to ensure that the value-add being articulated by the CVC has actually been provided.

6. Exit Potential

A common concern around taking capital from a CVC is whether it could hinder the startup’s ability to optimize on exit through potential misalignments of interest. Conflicts could include selling product or selling the company to a competitor of the CVC.

Each CVC handles this differently, and this should be a serious discussion point prior to closing an investment. Of our survey respondents, only 1 in 4 CVCs have acquired a portfolio company, only 12% of our CVC group note they regularly include a right of first refusal clause in the case of an acquisition, while 80% responded that they do not put any limitations on exit scenarios.

Corporate VC will likely continue to see many new entrants in 2016, a positive for entrepreneurs looking outside just traditional venture capital as a large number of corporations are seeking avenues to innovate. To optimize on the right CVC partners will require thinking through fit by considering the points above.

Special thanks to Rohit Jain (@RohitkJain) and Andrew Goldner (@agoldner) for support.

_______________

Samir Kaji is a managing director at First Republic Bank, where he leads a team managing venture capital and startup company relationships. He has spent over 15 years working within the venture capital industry. During this period, he has assisted and/or advised over 600 companies and 300 venture capital firms. Prior to joining First Republic, Samir spent thirteen years at Silicon Valley Bank, where he completed over 400 debt transactions, totaling over $4B in committed capital. Since 2008, Samir has led teams focused on providing services to venture capital firms and directly led engagements with several of the leading venture capital firms in the industry. Samir also has been an active angel investor in both venture capital funds and early-stage companies. Samir is a graduate of San Jose State University, where he earned his bachelor’s degree in finance, as well as Santa Clara’s Leavey School of Business, where he earned his M.B.A., with a concentration in finance.

Samir Kaji is a managing director at First Republic Bank, where he leads a team managing venture capital and startup company relationships. He has spent over 15 years working within the venture capital industry. During this period, he has assisted and/or advised over 600 companies and 300 venture capital firms. Prior to joining First Republic, Samir spent thirteen years at Silicon Valley Bank, where he completed over 400 debt transactions, totaling over $4B in committed capital. Since 2008, Samir has led teams focused on providing services to venture capital firms and directly led engagements with several of the leading venture capital firms in the industry. Samir also has been an active angel investor in both venture capital funds and early-stage companies. Samir is a graduate of San Jose State University, where he earned his bachelor’s degree in finance, as well as Santa Clara’s Leavey School of Business, where he earned his M.B.A., with a concentration in finance.

Jessica Peltz-Zatulove is the Principal at kbs+ Ventures, where she focuses on early-stage investments in digital media and marketing technology. Prior to joining kbs+, she specialized in helping connect marketers with emerging technology and spent 10+ years working with Fortune 500 brands including Verizon Wireless, Kraft Foods, and H&M. At Evol8tion she brokered numerous first-to-market startup and brand partnerships, and as a VP at Zenith Media was recognized an industry pioneer in the mobile space. Jessica has a BA from Indiana University’s Kelley School of Business, with a double concentration in marketing and international Relations.

Jessica Peltz-Zatulove is the Principal at kbs+ Ventures, where she focuses on early-stage investments in digital media and marketing technology. Prior to joining kbs+, she specialized in helping connect marketers with emerging technology and spent 10+ years working with Fortune 500 brands including Verizon Wireless, Kraft Foods, and H&M. At Evol8tion she brokered numerous first-to-market startup and brand partnerships, and as a VP at Zenith Media was recognized an industry pioneer in the mobile space. Jessica has a BA from Indiana University’s Kelley School of Business, with a double concentration in marketing and international Relations.

All information in this article is from sources deemed to be reliable.

The views of the authors of these articles do not necessarily represent the views of First Republic Bank.

©First Republic Bank, 2015