Financial services incumbents along with early-stage startups and large tech companies are all competing in fintech. CB Insights CEO Anand Sanwal gave a 110-slide presentation at our fintech conference in New York. The full deck covered broad VC funding trends for fintech and the developments in large categories such as wealth management, blockchain, remittance tech, and insurance tech.

On robo-advisors, Sanwal noted that market volatility has not necessarily been a boon to the category.

“It’s not all roses,” he said. “There are headwinds … When market volatility picks up, people want to talk to an advisor.”

At the end Sanwal highlighted 9 trends we’re watching that are generating excitement. The slides for those trends are included below.

1. Finance and banking chatbots

2. Peer-to-peer insurance

3. Foreign investors bet on US fintech

4. AI-driven hedge funds

5. The underbanked

6. Large tech companies wade into payments

7. Real estate crowdfunding

8. Digital-native banks

9. Fintech applications for blockchain

Transcript

Anand Sanwal, CEO, CB Insights:

So I’m gonna talk a little bit about the future of Fintech. We’re gonna cover lots of ground. It is 110 slides. Promise to go quickly. If you have questions, please use the hashtag. Use it on Twitter or on the mobile app, and I’ll try to get to them. Please ask me easy questions only. If you like something about the presentation, please tweet it out. If you do not like something about the presentation, please just keep it to yourself.

So, yeah. Let me jump in and we’ll go through this pretty quickly, I think. So this is what we do, take lots of data and try to predict technology trends. You’ve seen this join the conversation piece. We have lots of great customers, many of whom are in the room. So, thank you. I love you guys a little extra.

So this is kind of our mantra, right? Without data, you’re just another person with an opinion. So we’re gonna try to take a pretty data driven view of what we’re seeing in Fintech, and cover quite a bit of ground here.

How many of you are from I guess what folks would call legacy financial service firms, or incumbents? Okay.

How many of you like being called legacy financial services firms?

[laughter]

Okay. Yeah. I don’t know if incumbent is any better. I don’t know. They both kind of suck, in my opinion, but yeah. All right. How many are startups?

Okay. Investors?

Okay. Okay. So we have a pretty good contingent of corporates and investors. So the first part of this is just gonna talk a little bit about the pace of disruption. I hate to use the term, because it’s overused, but just the pace of advancement when it comes to technology more broadly. Then we’ll sort of apply it to what’s happening in Fintech, talk about some of the areas within Fintech that have been hot for the last few years, and then finally end with some of the nine trends that we’re looking at.

So when we look out using our data, some of the things that we think are interesting that maybe people aren’t talking a lot about today, but they are gonna be talking about in the next 12 to 18 months.

So if I just go to the next slide… So let’s just first talk about the faster pace of disruption. Who knows what this is?

All right. So fear of missing out. This first part is maybe a little bit more oriented towards the corporates, or for those of you who prefer to be called legacy. So this is fear of missing out, right? So we find, when we work with the corporate clients and they use our data, they use it in one of two ways. Some of them are motivated by FOMO, so Fear Of Missing Out.

Some of them are motivated by this. Anybody know what this one is?

So this one is fear of getting screwed.

These are very different personality types, right? Fear of missing out is sort of an optimistic view of the world. Technology is going to be big, and we want to be out in front of it and use it to enhance our business. Fear of getting screwed is sort of the scared view of things.

So this is a theme that I’m gonna try to hit upon a little bit. For those of you, again, who are with large corporations, I think it’s one thing that’s working thinking about, is what motivates your organization. We see companies that start as FOGS and eventually move to FOMO, but it is an important driver of how you think about innovation in technology.

So we’re gonna start with some very basic things, right? There’s a lot of startups in innovation, and you’re gonna hear this conversation around unbundling of the bank or of insurance, or other verticals, a lot over the next few days. So let’s just kind of define a few things.

So here’s Steve Blank’s talking about, startup is a temporary organization. Eric Ries has a human institution under conditions of extreme uncertainty. So when you think about it, startups are experiments, right?

So for a lot of big institutional or big legacy financial services clients or firms, they are outsourced R&D, right? So what you see here is, in the last last five, the number of early stage financings that have happened within… Across sectors. Not just Fintech.

But what happens with these companies that are sort of experiments today is, over time they become… And this is sort of the famous Clay Christensen disruption model… Over time they become more sophisticated. Their performance increases, and eBay, which started off for Beanie Babies and other things, kind of climbs up, and you can sell art and other things on it.

So this path has been well worn by other folks. So this is happening more and more.

One thing, I know I see folks taking pictures. You’re welcome to do that of the slides. These are all gonna be available to you in the mobile app, and we’re also gonna be sending out all the vignettes, as well as these slides. So just that heads up there.

This is also the other big seismic shift that we’re seeing within the corporate landscape. It’s harder than ever to stay on top, right? So this is the lifespan of the SNP500. You see a pretty dramatic shift down to 12, 13 years now… Your timeframe, or your time to stay in the SNP. So things are moving very quickly, and the threats, really, are multiplying.

So this is a great slide by the folks at Upfront Ventures that shows the cost of launching a startup, and it has probably come down even more since 2011. So what you have now is lots of experiments being created. Technology adoption is quicker than ever. This is an awesome graphic.

So if you look at the telephone, which starts in 1900 as that orange line, and you look at how long it took, it took 105 years for it to get to 90% adoption, and then you look at the cell phone or you look at the internet, right?

The pace at which technology now is adopted is remarkable, and it’s something that’s important for those of you in the audience who are thinking about how it might impact your business. Even within [inaudible 00:12:06] high fliers, the rate of growth is remarkable. So what you’re looking at here is, Facebook, by any stretch of the imagination, was an amazingly fast growing company, and you look at WhatsApp… Just kind of blew it out of the water.

So the pace even amongst the best has really accelerated. This isn’t a tech industry thing, right? So when you look at the hospitality area, you have Airbnb. You can imagine everybody at Marriott and Starwood and everywhere else is talking about Airbnb.

These are known for these unbundling graphics. There’s PNG, there’s FedEx, there’s the hotel, there’s the automobile, and then there is, of course, the banks. So this is Wells Fargo’s website, and all of the startups that are sort of taking little slices of it, or attacking it on various slices.

It’s not just a U.S. thing, right? So this is HSBC, along with some of its European death by a thousand cuts that are happening. So this is kind of… I used to work at American Express, and we used to spend a lot of time thinking about Capital One or Visa or MasterCard. So we were always looking at basis points, right? Share between one another.

Sort of the King Kong versus Godzilla dynamic that we worried about.

It’s really this death by a thousand cuts, right? These other folks that are worried, they want to take a comma out of your revenue. They are not looking at basis points, right? This is this unbundling thing that we talk about. This is what we’re talking about when we speak of that.

If I just go back to the fear of getting screwed mindset, right. So we hear this a lot from financial services. Incumbents is… These are all the reasons why startups will fail, right? They don’t have our balance sheet. Our brand is trusted. They don’t understand the regulatory environment. Whatever it may be.

The reality is, most startups fail, right? So if you look at this next slide of the funnel, right? Of the number of companies that get seeded, very few come out. So it’s sort of intellectually lazy to say that the startup won’t work, because most of them won’t work. That’s the nature of startups.

But the reality is, a bunch of them will not work. So if you look at retail, right, I had the distinct pleasure of working at Cosmo.com, right? So if you ever ordered Krispy Kreme donuts at 1:00 in the morning and nothing else, thank you for putting me out of a job.

So these are all of the companies that didn’t work, but the reality is, it’s the two or three or the one that works that becomes the problem, right? So if you look at CPG companies, you look at Macy’s, they are maybe late to the game, but they are thinking about Amazon in a big way. So for those of you who are financial services incumbents in the room, who is your Amazon? Who is your Uber?

Who is that going to be? There’s going to be lots of casualties. But you can’t take solace in the fact that lots of startups die. It’s the one that makes it that becomes the problem.

So your organizational mindset determines how you respond to this, right? Are you playing defense, or are you playing offense?

So that’s sort of the high level view of how things are going, and how we think organizations should be thinking about this. This is a little bit more of the state of the union of Fintech. So financial services, massive part of the U.S. and global economy you can see here as a percent of U.S. GDP… Kind of just how much it’s climbed.

So you have a big market. So investors and startups kind of see that. What you notice is that financial services firms haven’t necessarily kept up to date on technology, on demographic trends, on customer service expectations. So this is an opportunity for all these companies, right?

This is how much of these various industries are internet or not internet enabled, and you can see financial services doesn’t look very pretty here. Here you see how mobile and the distribution that it offers lets people, or lets upstarts, get distribution very quickly. So this is just private VS backed apps that are in the top 100. So, again, kind of a change in how things are distributed, in how you build a relationship with the customer.

Then you have the much talked about millennials, right? So I won’t read all these stats to you, but you have a demographic shift in terms of how people are thinking, and they are thinking differently about finance and their financial services providers.

Then the last dimension is on the services side, right? So when you look at the net promoter scores of various sort of financial services firms, they are not… Three. Like, I don’t even… Even if you don’t know what scale this is on, you know that that’s not good, right?

So the best, I think it got to, what, 64? Which is credit unions. They are doing very well. Then you look at some of the upstarts, right? So, have much more favorable ratings. So, again, this idea is that, how do you engage with customers in a different way? You see some of the new technologies out there that are doing that.

So Jamie Dimon, along with many bank CEOs, has talked about Silicon Valley as coming. I think the only thing I would take exception with here is that it’s really not just Silicon Valley. Obviously the Valley is the epicenter of this, but we’re seeing tons of innovation in Asia. Actually, we’re seeing a lot of financial services firms here look at what is happening the Asian investment community, because they think those models may eventually emerge here, right?

In Asia, where you have many areas where there’s no bank infrastructure and there’s no branch infrastructure, right, how is what they are doing eventually going to come here? You think about millennials here who don’t want to go to bank branches.

So technology is coming. Silicon Valley is obviously a driver, but it is beyond just the Valley.

So banking’s Uber moment, right? So this is looking at Netflix and other folks that disrupted travel music and video. Is that going to happen, and what is going to drive that? It’s the big question.

Goldman put out a report looking at the lending profit pools that were at risk, and we’re looking at massive amounts of money here that are at risk, and that, obviously, when you see values that large… You have the venture, private equity, hedge fund, etcetera, community that gets interested, and obviously entrepreneurs are interested in that as well.

So we see that in the numbers, right? $34.4 billion has been invested in Fintech companies in over 3000 deals since 2011.

The number is going up, right? So this is deals and dollars. The blue is the deals. The green is the funding. The more important metric here is deals, right?

Funding, a couple of unicorn rounds can distort that very quickly. Deals is really what’s important, right? That shows the buoyancy and vibrancy of the market, and you see that’s been climbing. A little bit of a hiccup in Q4 ’15, but that was broad based, and it recovered nicely in Q1 ’16, unlike in other areas.

You see a little bit of a regional difference. North America, Asia holding strong. Europe is sort of flat, but the numbers are just not impressive, right? Just to be very frank. So we see a level of aggressiveness from U.S. and North American financial services firms, as well as Asia based ones, that we don’t necessarily see from some of the European incumbents.

So the numbers, from a financing perspective, reflect that.

Big financings has obviously come down. You see a goose egg for Europe here, but in terms of $50 million financings too, the Fintech space have been pretty steady. They have come down, but if you look back on a longer time frame, this is actually very high versus historical norms.

Then for a lot of you in the room, and there’s lots of corporate VCs in the room, the amount of corporate participation has climbed pretty significant. So we see that. Startups have become outsourced innovation for lots of big legacy firms. So we see that.

Coming up, we see every week, Id’ say, a new firm saying, “Hey, we’re thinking about starting an innovation group, or a corporate venture unit.” So that is evident here in the numbers.

This is the big banks and their investments. So this is in the last, I guess, subsequent… Last five quarters, Goldman, City, etcetera, sent [inaudible 00:20:55] stepping up. But it’s kind of broad based. Not necessarily as active as some of the people at the top.

But you see the list is pretty significant.

This is investment just to Fintech companies. So if they are investing in other non Fintech areas, then this is not included in these numbers.

It’s not all good news, or maybe, depending on your perspective. Unicorn birth rate has declined. So this is a public health warning, of sorts. So there haven’t been any new Fintech unicorns in the 2016 year to date. So a bit of a headwind. That’s not Fintech specific. That is, financing market has dried up, or has tightened up. I shouldn’t say dried up by any stretch, but it has definitely tightened up.

Here’s the Fintech unicorns by sort of category. So you see payments and lending dominate. That’s the blue and the orange.

Insurance has been picking up steam. So that’s in the other category. But a lot of those others are from the insurance group.

Another obvious headwind is the public performance of some of the Fintech companies that have exited and IPO’d. So it’s not been pretty. It’s OnDeck, Lending Club, Square. None of them have done particularly well, right? So when you see that kind of performance, that obviously doesn’t inspire necessary confidence of investors.

Then, generally, VC backed Fintech exits have been… If I draw a generous trend line, they have gone up a little bit. But it’s not a great picture here from an exit perspective.

One of the things that we think is really useful is looking at where the smart money is investing. So smart money is a handful of firms that we think of as your top decile, so your Sequoias, your Accels, your Greylocks. Where are they putting money? So when we look at their trend, on the optimistic side, we see them continuing and actually looking at their pace to increase their investments year over year.

So Fintech remains an active area of investment amongst the smartest investors who have a track record, and where are they investing? So this is a tool on CB Insights called The Social Graph. What you see is, when we map out the investments of those smart money VS, a couple of themes emerge. Real estate, alternative lending, insurance tech, institutional investing tools and data.

Obviously we are investing in more than that, but when we try to pick out some themes using the Social Graph, those are some of the common ones that we see amongst the smartest private market investors.

So I’m gonna take a little bit of a detour, go a little bit deeper now on a few areas that have been talked about. Then we will end with the trends, and again, Q&A, please put through on the app or on Twitter.

So we’re gonna start with Bitcoin and block chain. We’re gonna be talking about this a little bit more later. So this is a high level… Fred Wilson is gonna be here talking about his views on it. So the price of Bitcoin has climbed pretty significantly, highest since 2014. This year we crossed a billion dollars, invested in Bitcoin, block chain startups on a cumulative basis. So a big marker for that world.

But what we see here is that the interest has shifted a bit from Bitcoin to block chain. So this is a tool on CB Insights called Trends. So we mind media chatter, and what you’re looking at here is the number of media mentions over time of these two things. We will dive into a little bit where blockchain is getting interest.

So blockchain has lots of applications, and you can actually use this media chatter to see where people are talking about it most.

This was… The Economist used some of our data to just sort of prove out not just the media, but the actual investment into Bitcoin and blockchain is going in slightly different directions, as you can see here.

block chain has become a pretty desirable area amongst the corporates. So you see, in the top five largest block chain chains and Bitcoin deals, corporate participation is really ramping up. So it’s one of the hottest areas, I would say, amongst financial services firms, whether it’s insurance, banking, payments companies, across the board. Folks are very interested in what’s going on in block chain.

Then there’s incredible diversity. Again, if just take this snapshot of the social graph, these are all of the different financial services players who have made an investment in blockchain and Bitcoin, and you see everybody from the payment networks to New York Life on the insurance side, to big banks. So it’s incredibly diverse, and then obviously folks at Google Ventures are here.

So everybody is really clamoring to understand this space and get access to it.

Wealth management personal savings. The robo advisors, we have John Stein here later today. This Y axis here is on a logarithmic scale. So the automated investment services are still a real drop in the bucket relative to these other categories.

Expectations are that they are gonna grow to be pretty material by 2020.

Investment continues in this space. So you see, here’s some of the folks that have raised, and here’s some of the recent funding announcements for those folks. So it continues to be a hot area. They have both grown. Wealthfront and Betterment are two of the better known robo advisors on the private side. They have grown their AUM both relatively quickly. Betterment has kind of exceeded Wealthfront recently. So you see that here as well.

But it’s not all roses. So here the AUM growth is slowing of both of them. So there are headwinds. One of the things that we have seen recently is when market volatility pick sup, people want to talk to an advisor. So how does their model work in that case, right?

So when the market is sort of steady and going up, everybody is happy, right? When things aren’t, that is when they want to talk to somebody. They might just want to be consoled and told that, probably don’t worry about what happened every day. But people are listening to, I don’t know, Mad Money or whatever. So they get spooked.

Incumbents have taken action as well, right? So this is, I think, one of the best examples. There’s this sort of knowing versus doing gap that we see amongst big incumbents. Big corporations are amazing at PowerPoint, right? They are really good at decks about a space. Like, amazing decks. I used to make them at American Express.

But then the doing part is where it gets harder, right? So, okay, I have all of this knowledge. But am I actually gonna put some money behind it? Am I gonna put a team behind it? Am I actually gonna do something about it, or are we just gonna present all day long, and watch somebody else do it?

In the case of the robo advisor space, you actually see Vanguard and Schwab actually did something about it, and very quickly they have seen results, right? They have a brand. They have a customer base. So, again, great example of not just knowing, but actually doing something about it.

Then you have startups like Acorn. So this is kind of savings rolling into the robo space as an investment. Still early days, but from an AUM comparison perspective, it’s still relatively small. But obviously, see a big number of accounts. So you’re looking at very small accounts in general, but again, targeting that millennial base is something that a lot of financial services firms are trying to figure out, and Acorn’s is an interesting model in that regard.

This is one of the concerns about robo advisors, or building a standalone robo advisor, by CEO of Morningstar basically saying, “You need a massive asset base to justify being in this business,” right? It costs a lot to acquire customers. You’re making very little per dollar that you manage. So it’s a volume game.

That’s one of the challenges in this space.

So given the scale requirements of the robo advisor industry, those that haven’t been able to show scale have been gobbled up, right? Relatively small AUM for most of these companies, but maybe there’s a technology or a team that folks could pick up. So you see some of those acquisitions that have happened already in the wealth management space.

I’m gonna turn a little bit to payments and remittance tech. Earlier this week, PayPal entered the fortune 500. Or, I think it’s the S&P 500.

But you see different areas that they are targeting. So we’re just gonna talk about some of the areas within PayPal’s world, or just payments in general. This is Venmo. How many of you use Venmo, right?

So if you listen to, there’s a podcast that just talked about Venmo and the whole social aspect of payments. I forget what it’s called, but really interesting, growing area for PayPal… I think doesn’t necessarily get as much attention, or starting to get, I think, a bit more attention. So kind of an interesting area for what PayPal is doing.

When you look at the payment processors, Stripes is obviously one of the darlings in this world. But if you look at Adyen, again, this is CB Insights Trends. It doesn’t get nearly as much press love, and doesn’t have the Silicon Valley Y combinator lineage, but is processing massive amounts of transactions now.

What we see here is early stage activity remains strong into payments. So, again, if you look at the deal trend here, seed series A deals continue to climb. So really healthy area. Money transfer, just changing gears a little bit. Really doing well.

Again, focus on the deal trend and less on the funding amount, because we think that’s a better indicator of the health of the market.

This is kind of, within the money transfer space, what you see here is, in relatively short order transfer wise has made it onto the table, the league table. Obviously, Western Union, that is a massive institution. So there’s a long way to go. But you do see a venture backed company there.

When we look at sort of the payments processors, you’ve got Visa investing in blockchain payment processing, MasterCard doing mobile commerce. block chain… Again, common theme, and Amex doing payments, blockchain… Amex takes a bit more diverse stand, I think, on its payments. They will invest in things that maybe are a little bit more tied it their consumer brand as well.

Insurance tech. Matt covered some of this this morning, but it’s this idea that insurance hasn’t kept up massive amounts of money that Matt alluded to earlier today.

Big expectation shifts here when it comes to consumer expectations, the ability to buy insurance, and then there’s really just an issue of product relevance, which we’ll kind of dig into. So this is… Nobody really loves their insurance company, is what this tells you.

Most of it is still happening offline. Then you have individual life insurance policies that are declining in terms of how many they have purchased. So thinking about new products that should be in the insurance realm is becoming increasingly important.

So because of those factors, demographic product service shifts, funding into insurance, and given the massiveness of the market, we see lots of funding flowing into this space. Three of the five largest Fintech fundings of late have been in insurance, and Oscar… Mario will be here tomorrow talking about what Oscar is doing. So some really interesting things happening in that space.

Most of it is at the early stage. So we talked earlier about experiments. There’s lots of experiments happening right now. So if you’re an incumbent in this space, these are the companies to pay attention to.

Again, not because they are gonna all succeed, but because they are an indicator of maybe where the world is going.

This is that landscape Matt showed you earlier. The corporates have really gotten active, and it’s across the board. Life insurance, re-insurers, a lot of the Chinese based insurers are getting active. It’s auto, etcetera. Really, across insurance, the level of interest is really, really widespread, and it has been very interesting to see… I think insurance gets… Daniel from Lemonade did a pretty good job, I guess, if I could call it that, of painting a picture of this very slow moving, archaic industry.

I have to give them credit for at least trying experimenting with investments and things. So we’re seeing a lot of activity there, which has been good.

Connected IOT devices to help people with underwriting, and actually claims prevention. So this is an interesting idea now of not just making it about claims, but how do we actually make it so you don’t need to file claims, right? How do we help you avoid that?

So re-insurance… So this is, I think, Munich [inaudible 00:34:23] and Swissery [SP] getting involved. Lots going on there.

So I’m gonna close with more speculative things that we’re watching. I think I talked to somebody who actually… I saw some folks with their name badges had some of these, so that was cool to see.

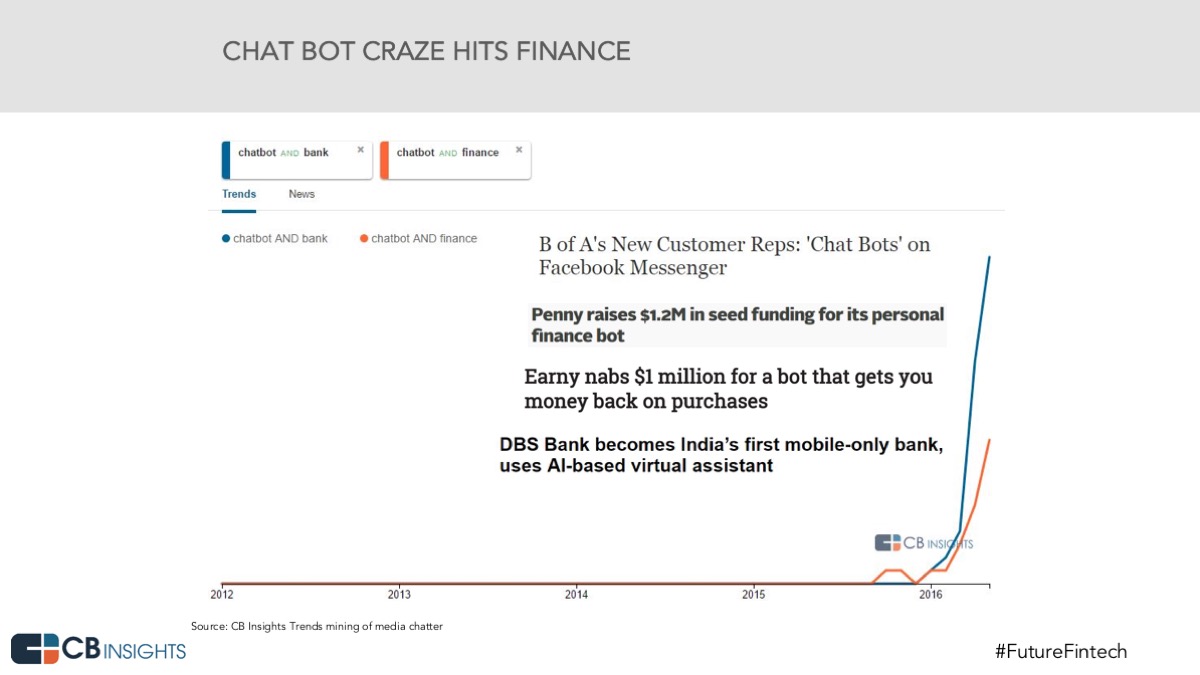

So chat bots hitting finance, right? So on trends we did a search of chat bot and the word bank appearing together, or chat bot and the word finance appearing together. So you see a little bit of a step up there, and some of the articles talking about this.

So this is one of the trends that we think is going to be interesting from a customer support perspective, or personal finance management perspective. We think there’s going to be some interesting companies and things happening there.

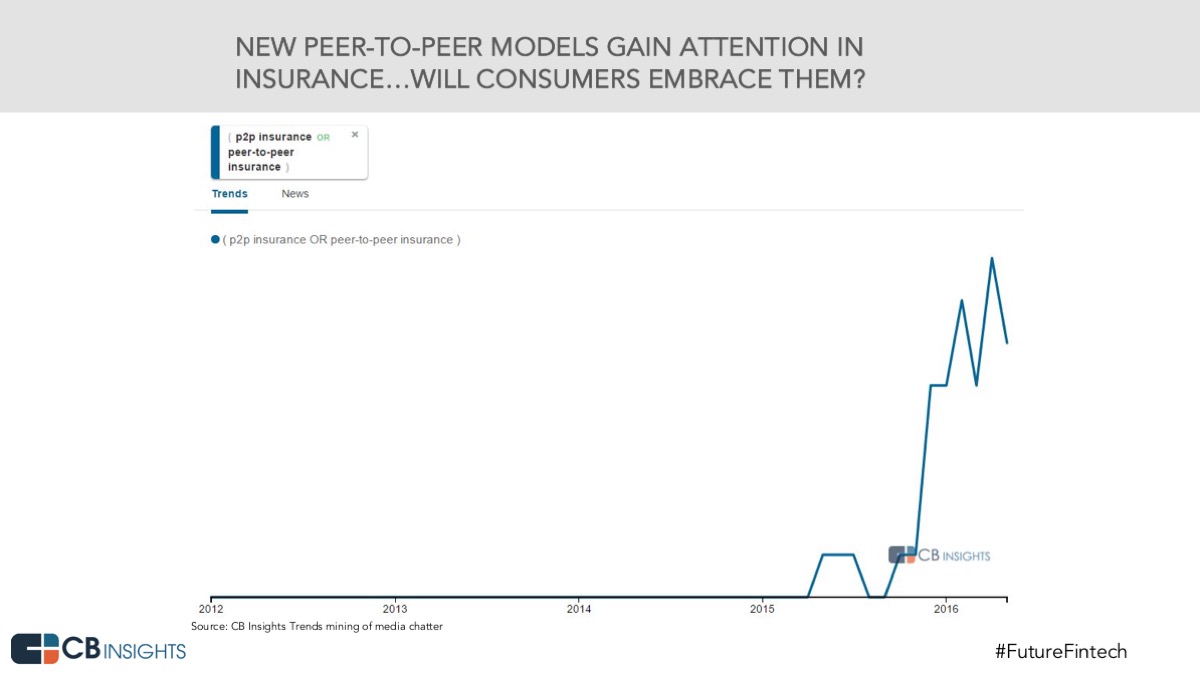

The next thing, peer to peer models and insurance. So Daniel at Lemonade is a great example of this, but again, using trends, we can look at what’s been happening in insurance when we look at insurance in P2P models. So, again, heightened interest in that area. It’s still early days, so we’ll see what happens there.

But we think of it somewhat analogous to P2P lending, right? It starts out and didn’t get maybe a ton of attention, and then quickly took off.

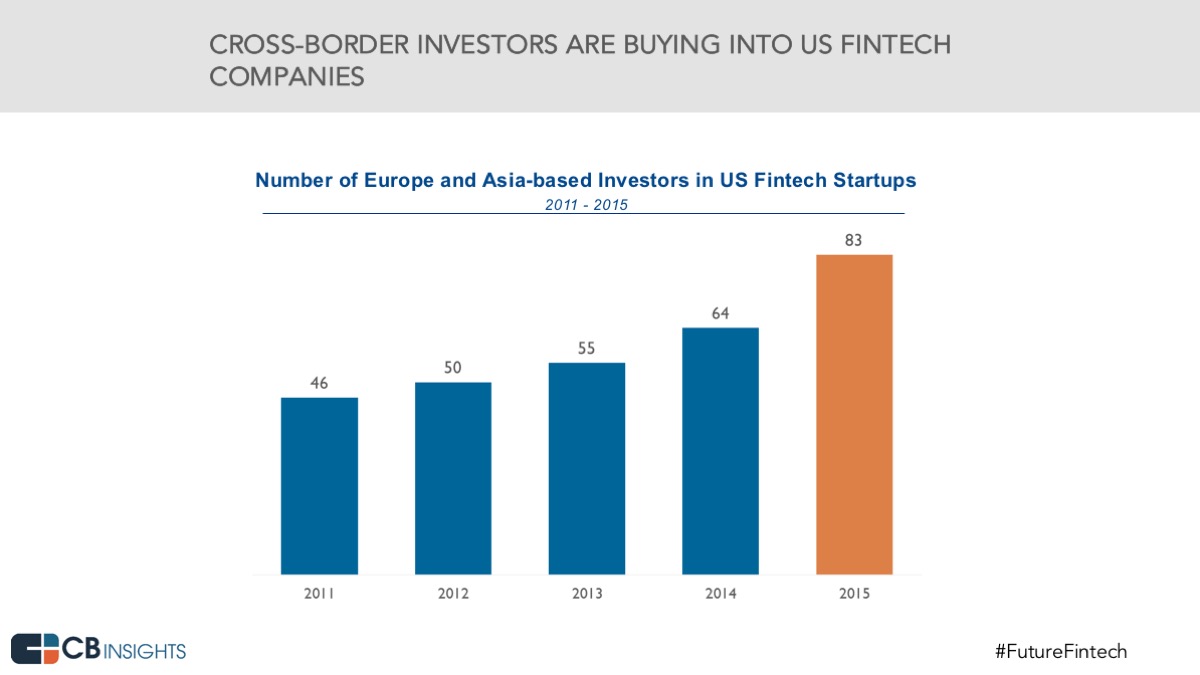

This one, I think, is interesting. A lot of non U.S. investors are investing in U.S. Fintech startups, including a lot of Asia based corporations. So this cross border investment activity is one thing that we think is probably going to intensify when we look at Asia as a market, and it’s an amalgamation of lots of smaller markets, obviously. But the level of aggressiveness in terms of wanting to access innovation and invest is really unlike anything that we’ve seen since we began the company.

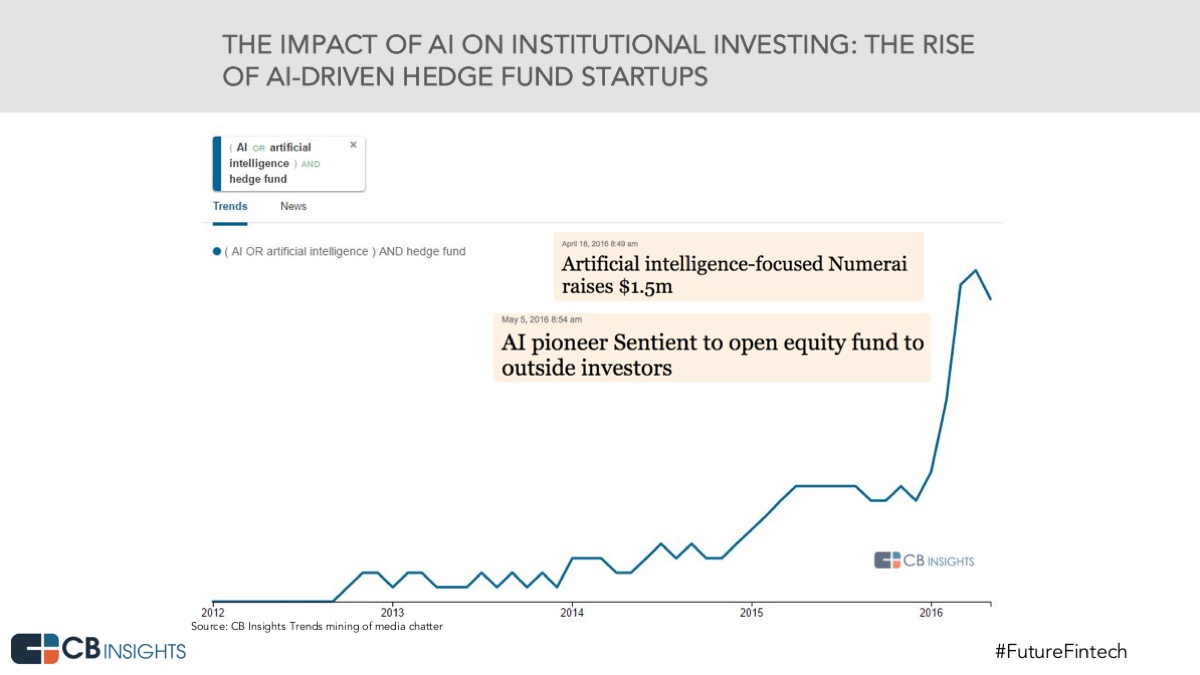

AI on institutional investing. So artificial intelligence is the buzz-iest of terms. I presented at the CEO… Portfolio company’s CEOs were there. I think one of our clients… I presented at their CEO summit. My advice to them was, when you’re doing your next round, just throw artificial intelligence somewhere in your pitch deck. It’s sort of that hot. It’s sort of the new big data.

So when you’re on the buzzword bingo scale, it’s off the charts right now.

AI, with regards to AI driven hedge fund and institutional investing… Another trend we’re looking at.

Underbanked, we’re gonna talk about this tomorrow. I then folks are starting to maybe come around to this as being an opportunity that, actually, you can build real businesses in. I think three, four years ago when we talked about the underbanked with clients, they sort of nicely told us, “Yeah, we think that’s interesting, but it’s probably more for the impact investors. It’s not necessarily for us, because we care about profit.”

That’s changing. So that has been interesting to see. It’s a segment of the market that’s not, obviously, hasn’t gotten as much attention, but is massive.

This is one that I kind of really like. So this is a little messy in trends. So what I did

was just look at Amazon, Google, Samsung or Apple, any one of them mentioned in an article along with mobile payments, and then I looked at Amex, Visa, MasterCard and Citigroup along with mobile payments, and you see, actually, a lot more chatter amongst tech big boys in this area of mobile payments.

So it’s interesting. I think Dan Reed from American Family Ventures mentioned it earlier, and we’re gonna talk about it, I think, with Samsung and Microsoft tomorrow… Is being a bit leery of working with big tech companies, right? So I think that’s an interesting dynamic. It’s no longer just Citigroup versus Bank of America. But it’s, you know, you have Amazon and Google and all of these unusual suspects entering.

So I think that’s an interesting trend that we’re tracking in terms of their level of activity, stepping up within Finservices or Fintech in general, and then within payments.

Real estate has become a big area of growth, and sort of crowd funding, tracking, how is this going to take shape?

This is not we [SP] work, right? We’re not talking about space. We’re talking about actually the funding of real estate. So we think this is a pretty interesting area that we’re still early days tracking.

Digital challenger banks. Some chatter about this, but the actual idea of online only banks, how those are going to work and take off… So an area of interest that we’re tracking.

This is the final one around block chains. So blockchain is very interesting. It gets a lot of chatter. But then we tried to look at, okay, where is block chain being talked about? So blockchain versus in insurance versus capital markets versus remittances versus compliance versus lending, and you can see, without saying who is one, two or three, what you see is all of them are going up, right?

So the interesting thing about blockchain is all these disparate applications of it, and disparate industries that people are talking about deploying it in. So we expect, and we’ve seen it in media and music, and all sorts of other non financial services areas that folks are talking about blockchain.

So that was everything I had. If there’s questions, I’m happy to take them.

But thanks again for your time, and I hope this was useful. Thank you.

[applause]

Man: Yeah. There are a couple of questions. Is Fintech reaching a peak in hype, or is this just the beginning?

Anand: So I think you have to unpack Fintech. Fintech covers a lot of ground, right? It’s everything from marketplace lenders to robo advisors to insurance tech, to drones for property casualty assessment, right? So I think there’s areas that are maybe more hyped, and then there’s areas that are very much in the discovery phase. So if you look at the block chain example, that’s more, I think, early days.

If you look at marketplace lending, probably a little bit tougher slog right now. A bit more mature.

So Fintech is a sort of very broad category. Within that there’s gonna be things that are growing in interest and things that are declining. It’s hard to say that, overall, the area is hyped.

Man: We have time for one more question, but you talked about how corporates are dying by a thousand cuts. What are some ways they can brace themselves, or adapt to the changing landscape of Fintech, and are there certain things that they’ve done that work particularly effectively?

Anand: Yeah. So I think when we look at it… An important part of the process is knowing. So looking out and seeing what are the early stage companies, what’s happening in news media, and picking up on those signals early. So I think there’s a lot of insights that can be drawn from that.

Ultimately, though, you have to do something, right? You have to put money behind it, some initiative, whether it’s a company you want to invest in, whether it’s some skunk works you want to build out, whether it’s an acquisition. It’s sort of maybe trite advice, but you actually have to do something, right?

You can’t just talk about innovation and put board decks together about, we need to be worried about these companies. You actually have to invest and do something. But I think it does start with understanding what your competitors are doing, understanding what business models are emerging, what areas are gaining interest, which ones are not.

So I think it does start with that, but ultimately you have to put some money and some resources behind these initiates.

So, cool. All right. Thanks, everybody.

If you aren’t already a client, sign up for a free trial to learn more about our platform.