Has the surge of billion dollar+ tech exits, growing private company valuations and a booming venture capital financing market actually been a good thing for venture capitalists?

At the end of 2013, we analyzed billion dollar tech exits and the ability of VCs to get into those big exits consistently and early, and the results were not pretty. So unpretty, in fact, that we declared that most VCs are not great predictors of technology success (VCs loved that btw) We found that only 3.5% of active VCs had actually invested in 2 or more billion dollar exits over the 10 year period we’d studied (2004 to 2013). A single billion dollar exit was luck. Two or more was where an investor could be considered having skill.

At the time, we wrote:

While venture capitalists talk about wanting to identify and invest in billion dollar companies, the reality is that few VC investors actually do. Even when they do, very few are able to do it again … Moreover, for those who were astute enough to get into these big exits, getting in early is even rarer, highlighting the paucity of firms who can truly see around corners and who have access to truly superior dealflow.

What a year a difference makes. With the vibrancy of the market in 2014, things are most definitely looking up for venture capitalists.

We compared the ten year period from 2004-2013 versus 2005-2014, and there is some good news:

- More VCs had billion dollar exits – From 2005 – 2014, 161 VCs had at least one $1B+ exit in their portfolio, while from 2004 – 2013 only 104 VCs managed to get a Unicorn exit.

- The number of VCs with multiple billion dollar exits also grew – The number of VCs with two or more $1B+ exits nearly doubled. There were 38 (or 3.4% of all active US tech VCs) from 2004 – 2013 while 2014 saw 68 (5.9% of active VCs) score multiple billion dollar exits from 2005 – 2014.

- A higher % of $1B+ exits are being sourced early. From 2005 – 2014, of the VCs with two or more $1B+ exits, 24% of their exits were sourced at the Series A stage or prior. This figure was up versus 2004 – 2013 when 20% of multi-Unicorn VCs’ investments were made at Series A stage or prior.

Summary: It looks to be a good time to be a venture capitalist. Of course, the old adage that “one should not confuse brains with a bull market” is worth restating.

We dig into the data below in more detail.

More super-sized billion dollar exits

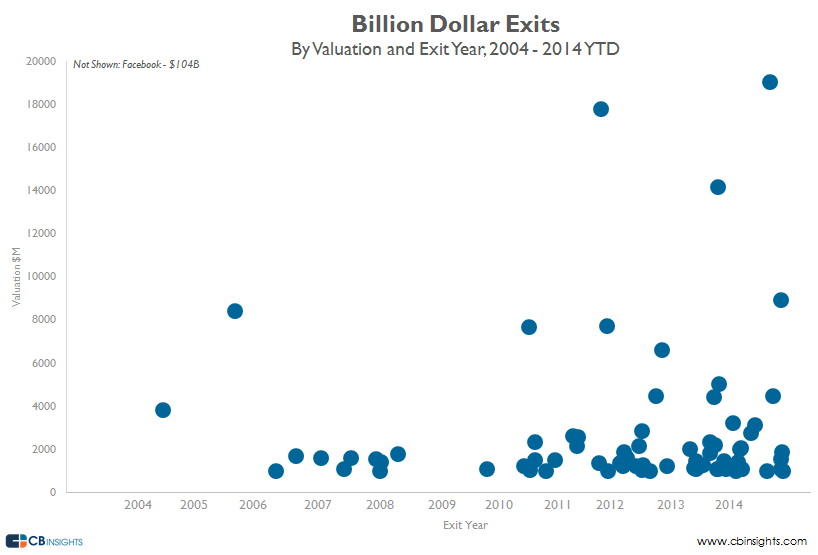

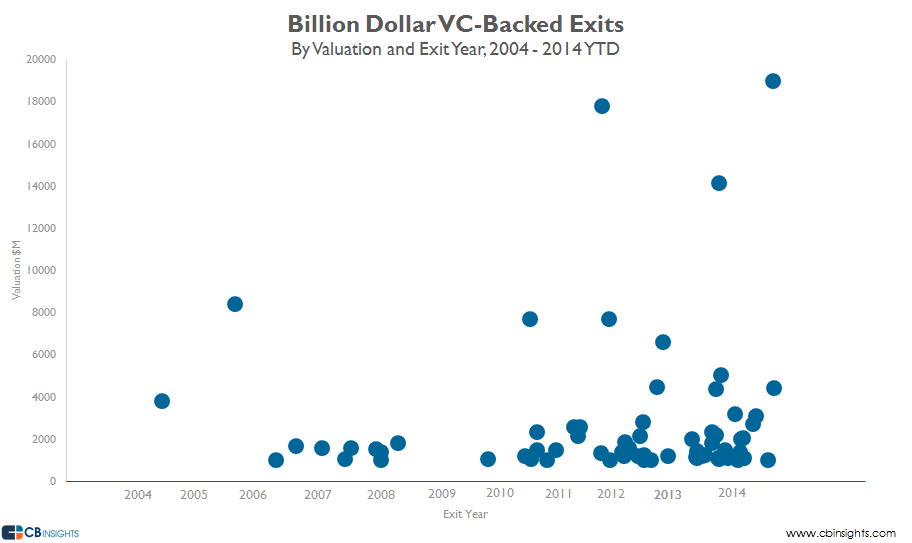

As the graphic below highlights, there has been an acceleration in the pace and number of billion dollar VC-backed exits. Billion dollar valuations to private companies have followed suit in 2014 with 38 private companies joining the billion dollar club in 2014. The chart below plots the exits (sans Facebook’s $104B IPO) by year and valuation. The dramatic increase in Unicorns is evident by the growing cluster that starts in 2012. Starting in November 2011 with Groupon’s IPO, we also see the increase in VC-backed US tech exits over $10 billion.

{kind=link}

{kind=link}

More Lucky VCs AND more Skilled VCs, too

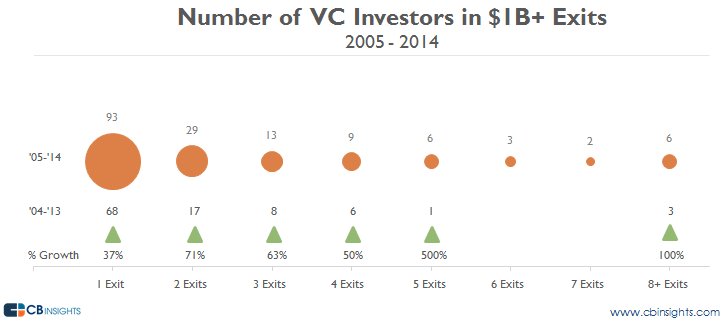

As mentioned above, 161 VCs invested in the billion dollar tech exits from 2005-2014. 58% of them (93 of the 161) invested in only a single billion dollar exit. These are the “lucky VCs” since we’ll reserve the “skilled VC” tag for those in 2 or more. On a sheer numbers basis, the number of VCs who invested in a billion dollar exit climbed significantly, as the image below illustrates. Our prior analysis which covered 2004-2013 shows only 68 VCs who had a billion dollar exit highlighting the 37% growth in the absolute number of lucky VCs (those with only 1 billion dollar exit).

The first bubble represents the 93 VCs who only invested in one billion-dollar company, which equals ~8.2% of all active VCs in US Tech. The next bubble, which represents VCs that had exactly two billion-dollar company exits, shows that the number of VCs who can invest in multiple unicorns are rarer, dropping sharply to 29 or 2.6% of all active tech VCs in the US.

As we move further to the right, we enter increasingly rarefied VC air. The far end of the spectrum is comprised of 6 VCs who each participated in 8+ billion-dollar exits, including Sequoia Capital, New Enterprise Associates, Kleiner Perkins Caufield & Byers, Accel Partners, Benchmark, and Greylock Partners. These six elite VCs represent just 0.53% of all active US Tech VCs.

The skilled VCs (those with 2 or more billion dollar exits) are increasing.

Of the 161 total VCs with a $1B+ exit, 68 have been investors in two or more Unicorns since 2005, up from just 35 between 2004 – 2013. The 2014 “skilled VC” figure is equal to 5.9% of all active VCs investing in US-based tech companies

Are these really the skilled VCs?

Being part of large exits is not enough of a test of a VC’s effectiveness. There is a lot of logo chasing occurring in VC today and so an investor who has jumped into later-stage companies (Series C or later) is not as skilled as an investor who got in early.

In other words, large late-stage exits do not necessarily correlate with the investment’s returns, as often the largest returns from an exit go to the earliest investors.

To that effect, and to better assess a VC’s investment selection proficiency, it is important to look at what stage they made their first investment in a company.

The chart above breaks down the investors based on the stage they invested in each of the $1B+ companies. For example, if we look at the six investors with 8+ $1B+ exits, we find that 60% of their investments were in a Series B or prior round.

On the other end of the spectrum, when looking at the 93 VCs with just one $1B+ exit since 2005, 47 (or 51%) were at or before the Series B stage. This number is up considerably from last year’s analysis which saw just 38% of the 68 VCs with one $1B+ exit get in at Series B or earlier. Said another way, nearly half of the VCs who had just a single billion dollar exit over the period from 2005-2014 were not able to get in prior to the Series B financing.

{kind=link}

{kind=link}

How many VCs actually see around corners?

When looking who invests at the Series A stage or earlier, we start to identify the truly great VCs. The elite “stock pickers” who have the best networks, the proprietary dealflow, the heightened sense of pattern matching.

As you can see below, across the entire spectrum, the number of VCs who consistently get in early to these deals is quite low. If you are an LP or entrepreneur, these are the truly elite and skilled VCs.

All of the underlying exit and investor data used in this research brief is on the CB Insights Private Company Exit Database. Sign up for free below and learn more about our VC predictive models, Investor Mosaic.

Methodology / Notes

For companies that exited via M&A, the valuation is the real or rumored valuation at date of exit announcement. For companies that IPO’d, the exit valuation was calculated using the closing stock prices on the day of the IPO.

The data comprised of exits that occurred between January 1, 2004, and on or before December 31, 2014.

Amazing unicorn image by Zoomar

If you aren’t already a client, sign up for a free trial to learn more about our platform.