The following is a guest post by Samir Kaji (@samirkaji), Managing Director at First Republic Bank (@firstrepublic).

Although it has been less than a year since I posted my primer on the micro VC market, there have been a host of major developments since.

Loosely, micro VC firms are venture firms that raise funds that share the following characteristics:

• Less than $100M in size (although most are smaller than $50M)

• More than 80% of initial checks are invested in seed rounds

• Invest on behalf of 3rd-party investors (LPs)

Over the past 18 months, I’ve met with over 150 micro VC managers of all sizes, geographies, and investment themes. Before I attempt to prognosticate where I think the micro VC market is headed, I want to share some of my recent observations.

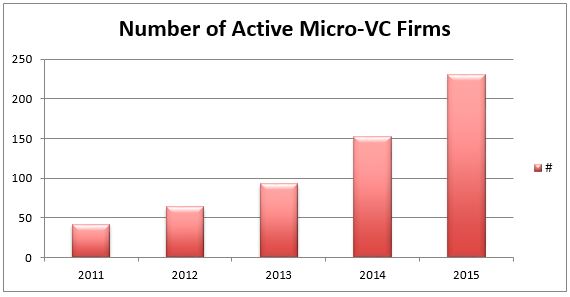

Growth, growth, growth

The table below, leveraging data from CB Insights along with SEC filings, displays the growth in the number of micro VC firms over the past five years (*2015 represents year-to-date numbers).

- Of the 236 firms identified, approximately 50% have not raised a fund over $25M. This number isn’t really shocking given the low barrier of entry at this size — the majority of these funds of this size are closed without any traditional institutional LP backing.

- Over half are located in Silicon Valley. New York, Los Angeles, and Boston together account for just under a quarter.

Rising bar for institutional LPs

As noted above, nearly half of micro VC firms have little to no institutional LP capital. Institutional capital for the micro VC market includes endowments, foundations, corporates, and fund of funds. With respect to fund of funds, many institutional fund of funds have been quite active over the past couple of years in micro VC, including firms like Venture Investment Associates, Cendana Capital, Sapphire Ventures, Weathergage Capital, Horsley Bridge, Northern Trust, SVB Capital, TrueBridge, Greenspring, Legacy Ventures, Next Play Capital, and Top Tier Capital to name a few.

Although many allocators are still exploring new micro VC managers, many have already placed their bets in the space, and the rise in numbers of new funds coming to market has made it virtually impossible to separate signal from noise.

Special purpose vehicles (SPVs)

Due to capital constraints, micro VC funds often struggle to take advantage of valuable pro-rata rights in future rounds of their most promising portfolio companies. As a remedy, micro VC managers are now very actively forming SPVs to enable pro-rata investing in top-performing portfolio companies. Keep in mind that SPVs don’t solve for fund-level economics as they are stand-alone entities outside the fund, but do offer LPs of a given fund the ability to participate directly into top portfolio companies at reduced economics. These SPVs include favorable (for GPs) deal-by-deal carried interest economics, unlike a fund where carried interest is paid on the entire portfolio. Check out AngelList’s comparison of deal-by-deal economics vs. pooled funds.

Thus far, most SPVs have been done through offline channels, but we’re starting to see increased use of platforms such as AngelList (syndicates) for SPVs.

Migration to investing later in the Seed stack

As discussed by many this year, the seed-financing landscape has become clearly segmented along the following lines:

- Pre-seed ($500K-$1M) – Good management team/market/solution, little traction.

- Seed ($1M-$2M) – Good management team/market/solution, early evidence of product-market fit and traction.

- Post-seed ($2M-$4M) – Same as above, but with fairly significant evidence of product-market fit and tangible business-specific traction metrics.

Over the past year, many micro VCs have continued to migrate toward Seed and post-Seed investing. This trend has resulted in a challenging environment for pre-seed companies seeking institutional capital, and perhaps not as intuitive, has created a higher bar for follow-on financing for companies that have raised large post-Seed rounds. To expand, most lifecycle investors today evaluate companies that have previously raised large post-Seed rounds though a similar lens as companies that have previously raised small A rounds, and therefore grade to tougher Series B-level metrics.

Graduates

With the prior two points in mind, many 1st generation micro VCs have gradually grown fund and team sizes. Firms like Data Collective, Felicis Ventures, and SoftTech VC have evolved into more conventional multi-stage investors that aim to drive value across all stages of development.

Internet and mobile dominate

Predictably, nearly 90% of capital invested by micro VC funds since 2011 has been deployed into the mobile and internet sectors. According to CB Insights, the top sub-sectors are:

Performance is strong

Take a minute to soak in the following numbers for overall fundraising:

- In 2014, nearly 211 rounds of more than $40M were completed

- In 2015 alone, nearly 50 US companies have raised rounds in excess of $100M.

- Over the past 3 quarters, 51 companies have joined the unicorn club of private companies valued at over $1B.

These growth rounds have created substantial performance bumps in the portfolios of micro VC firms. Most micro VC firms raising capital today maintain very persuasive performance metrics for recent vintages.

I’m regularly seeing Vintage 2013 micro VC funds that have net internal rates of return (IRR) greater than 25% and MoICs (multiple on invested capital) of 1.5-2.5x. While these largely unrealized numbers are compelling, they represent table stakes for managers hoping to raise in the current market.

Unicorn hunters

Contrary to what some have posited, unicorns (or more accurately, liquid unicorns), are essential for alpha returns — which is a 4X+ net return of capital. Here is a sampling of micro VCs that have invested in more than 1 Unicorn. SV Angel leads the pack with 16, although important to note that their velocity-based investment model provides for some skew.

The future?

Expansion, then contraction

In addition to the presently 236 active micro VC firms, I’m currently tracking nearly 30 firms that are raising freshman funds. My expectation is that we’ll continue to see expansion with the number of active micro VC firms peaking around 350. From there, I anticipate a steady contraction of active micro VC firms, with no more than 150 in 2018. A few factors will contribute to the contraction:

- Unstable LP bases: As mentioned, nearly 50% of funds are smaller than $25M. The majority of those funds have LPs that are non-institutional in nature. If history serves a an accurate proxy, non-institutional LPs, particularly small family offices and high net worth individuals tend to be unpredictable follow-on fund investors, particularly given the unlikely nature of significant distributions over the next few years, and the looming threat of a potential market contraction.

- Graduates: As covered above, several brand-name micro VCs have gradually transitioned to full-stack venture firms.

- Many existing micro VC firms raising in 2017 and 2018 will be in the market for their Fund IIIs. Outside of Fund I, Fund IIIs tend to be the most difficult as the fundraising dialogue emphasizes performance over promise.

Private secondary sales

Very few micro VC firms today engage in secondary trading of shares in late-stage expansion rounds. Several dynamics play into this including immature portfolios, difficulty in securing company agreement, along with the risk of sub-optimizing fund performance through premature sale. A few factors may force micro VCs to sell shares in secondary sales:

- Exits continue to get pushed due to the abundance of late stage capital.

- Pressure by LPs on distributions prior to additional allocations

- Risk mitigation: While firms may sacrifice upside by selling private securities prior to a true exit (IPO or acquisition), the specter of high flyers getting their wings clipped as more time passes looms as a real risk. Amplifications of risk includes stacking of preferences from future rounds, especially dangerous for early investors that have invested in high flyers that end up liquidating for amounts equivalent or less than aggregate capital raised (and let’s not even touch the topic of late-stage “down rounds” or recaps!). For GPs and founders alike, I’d highly recommend Heidi Roizen’s blog post around the capital stack.

Theme-centric firms

While the majority of first generation micro VC firms are Seed stage generalists, the raw number of firms has highlighted the importance of demonstrating differentiation through domain expertise, network, or brand.

A few examples include:

- Maven Ventures — Consumer

- Lemnos Labs — Hardware

- Learn Capital — Education tech

- Govtech — Government technology startups

- Bullpen Capital — Post-seed round investing

- Precursor Capital — Pre-Seed stage investing

- Rivet Ventures — Investing in companies that focus on markets heavily influenced by female decision making

- Forerunner Ventures — Commerce-focused businesses

- Luminari Capital — Media tech

- Ecosystem Integrity — Capital-efficient Cleantech

Online platforms

Micro VC firms are primarily structured as standard close-ended, 2/20 structures. Even most SPVs are done through offline channels. I’m expecting an exponential growth in the use of online platforms such as AngelList by institutional investors, both as a preferred avenue for SPV activity, but as a viable alternative to raising a traditional fund, particularly as data and network functionality emerge.

Sharp drop in pure accelerators

Over 200 accelerators exist globally today, and sell insight, community, and validation as value drivers. However, with the rise of co-working spaces and meet-up groups along with ubiquity of information, the notional value of pure accelerators has declined, and the best accelerators have become micro VCs (500 Startups, YC, Lemnos Labs, MuckerLabs). I’m anticipating a huge drop in the number of pure accelerators in the next 24-36 months.

Note: Thanks to CB Insights for the data and @Rohitkjain for culling through it.

____________

Samir Kaji is a managing director at First Republic Bank, where he leads a team managing venture capital and startup company relationships. He has spent over 15 years working within the venture capital industry. During this period, he has assisted and/or advised over 600 companies and 300 venture capital firms. Prior to joining First Republic, Samir spent thirteen years at Silicon Valley Bank, where he completed over 400 debt transactions, totaling over $4B in committed capital. Since 2008, Samir has led teams focused on providing services to venture capital firms and directly led engagements with several of the leading venture capital firms in the industry. Samir also has been an active angel investor in both venture capital funds and early-stage companies. Samir is a graduate of San Jose State University, where he earned his bachelor’s degree in finance, as well as Santa Clara’s Leavey School of Business, where he earned his M.B.A., with a concentration in finance.

Samir Kaji is a managing director at First Republic Bank, where he leads a team managing venture capital and startup company relationships. He has spent over 15 years working within the venture capital industry. During this period, he has assisted and/or advised over 600 companies and 300 venture capital firms. Prior to joining First Republic, Samir spent thirteen years at Silicon Valley Bank, where he completed over 400 debt transactions, totaling over $4B in committed capital. Since 2008, Samir has led teams focused on providing services to venture capital firms and directly led engagements with several of the leading venture capital firms in the industry. Samir also has been an active angel investor in both venture capital funds and early-stage companies. Samir is a graduate of San Jose State University, where he earned his bachelor’s degree in finance, as well as Santa Clara’s Leavey School of Business, where he earned his M.B.A., with a concentration in finance.