Microinsurance — like microloans and microcredit — is traditionally thought of as a product for those in the developing world who earn $4 or less per day. But the very same innovations that made microinsurance possible and profitable are about to transform the larger insurance market.

For global insurers, microinsurance has been a fast-growth market: from 76 million clients in 2010 to 260 million in 2013. (Lloyd’s estimates that potential global market at 1.5 billion to 3 billion policies.) To sell these products profitably, however, insurers had to become drastically more efficient in administering policies. Mobile apps, fintech systems, and other digital innovations made that possible.

I believe that as these tech and operational efficiencies saturate the industry, we’re going to see a burst of innovation in insurance that will lead to more flexible, consumer-centric products for everyone.

To understand why, you have to look at two major inefficiencies in how insurance works today:

Operational inefficiency: A standard $1 million term life insurance policy costs about $1,000. At that price, insurers can afford to have multiple humans touch each policy as it flows through departments, from underwriting to in-force, and into multiple IT systems. When policies earn that much revenue, it also makes sense for a company to improve its bottom line by increasing sales or competing on customer experience rather than driving down operating expenses. Microinsurance—where a premium might be just $10— required a new paradigm. An operations efficiency loss of just $1 per policy represented 10% of the total revenue.

Distribution inefficiency: The commission-based sales model in insurance depends on those large, expensive policies, which then fuel operational inefficiency. An agent who might get $1,000 to $20,000 in commission for selling large life insurance policies doesn’t bother much with selling smaller policies (e.g. renters’ insurance or smaller term life) that earn him just $10 to $100. The carriers then focus on the larger policies that can support the big commissions, and thus don’t care about improving operational efficiency. It became a cycle that was difficult to break until technology intervened.

Micro policies’ big opportunity

Metromile shows how innovative micro-policies are already popping up outside the traditional realms of microinsurance. The auto insurer pioneered the idea of usage-based car insurance, targeting the low-mileage driver: customers pay a low monthly base rate (10% to 20% of a standard policy) plus an additional charge per mile driven tracked via a telematics dongle. Metromile built its systems to be dynamic and efficient to automatically ratchet the insurance bill up or down depending on miles driven. Since Metromile proved the micro usage-based model, all major carriers have followed suit.

This is only the beginning. There are surely hundreds of ways to insure risk in a more granular way, with operational costs driven down by technology. Here are a few ideas I’ve been considering:

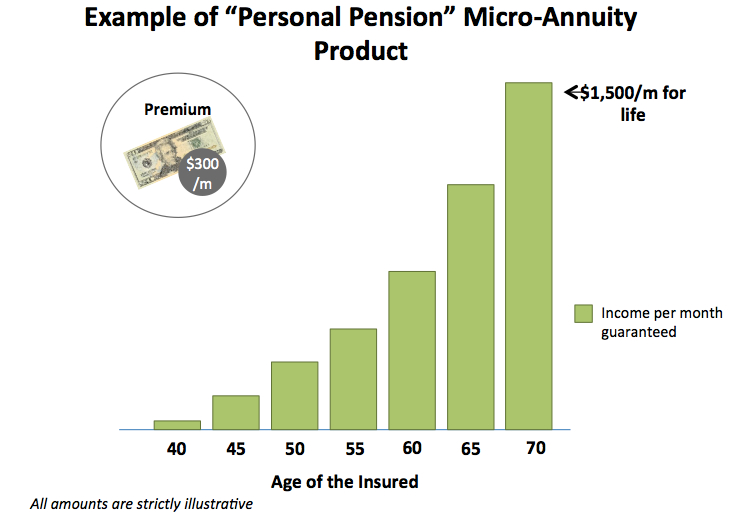

Micro-annuities/personal pensions: Annuities are insurance on longevity. Sold only by insurers, these policies help make sure you don’t outlive your assets, and they act much like a traditional pension by providing guaranteed income, for life, starting at retirement. Right now annuities are stuck in the large commission-cycle mentioned above; you won’t find an annuity with initial premium payments below $1,000. But I’m convinced that a micro-annuity, a “Personal Pension,” would be a big hit. I can’t be the only one who wants an advisor to handle contributions to a pension and show me exactly how much guaranteed income I’ll have at age 70. An asset-management fee eliminates the commission and a roboadvisor dramatically improves efficiency.

Automated insurance: The apps Digit and Acorns have demonstrated the allure of automatically siphoning off spare change or small payments and turning them into an investment portfolio and savings. Using a similar mechanism to fund disability, life, and long-term care insurance seems equally feasible. I would happily sign up for an automated tool that would systematically fund those needs over time, gradually increasing my coverage until I was appropriately protected.

Bridging insurance and debt: For much of the middle class, the breakdown of a car, refrigerator, or being unable to work for a few days can be a financial catastrophe. To deal with these sudden sub-$1,000 expenses, many people take out payday loans or accumulate credit card debt. Less than half of Americans report having the extra cash available to cover a $400 bill, and few people carry policies, such as mechanical breakdown insurance, that protect against these events. It should, however, be possible to buy a product that bridges the worlds of debt and insurance. This product would allow a customer to prepay against risk (prepaying would be cheaper on the whole because it removes credit risk) but allow for credit if the cost exceeds the amount insured. Frank, a New York-based mutual-lending startup, is already starting to facilitate products like this.

Fixing the efficiency gap

In my personal pension concept, both the operational and distribution efficiency problems are solved with a roboadvisor that automates sales, the processing of payments, calculating and collecting asset-based fees, and eliminating commissions.

One Financial, a portfolio company of AXA Strategic Ventures (ASV), could leverage the back end of its mobile finance operation to create the efficiencies microinsurance needs. One Financial has built a new, extremely efficient banking platform called Bee, which has a direct line to its clients via mobile phones. Their customers might, for instance, be interested in corpse repatriation microinsurance: a policy that would pay the $5,000 to $10,000 cost of returning a dead body from the U.S. to Mexico for burial. Partnering with a life insurer, One Financial could easily distribute, at extremely low cost, a micro-life insurance policy that would cover this expense.

There are other ways to eliminate some operational costs altogether. WorldCover, a recent Y Combinator company, is using a pari-mutuel insurance structure to create efficient and profitable crop and weather micro-insurance. Its simple system — pay if it doesn’t rain, don’t pay if it does — eliminates the cost of claims, administration, support, etc. This only works, of course, when data from a third party can easily verify a claim. For most of insurance, that’s not an option.

What are some other ideas?

The micro-insurance moment is upon us. The market is there, the technology is ripe, and there are countless ways insurance can mitigate the immediate financial issues confronting customers. At ASV, we’re aggressively seeking new ideas and partners to create breakthrough products, and I believe exciting things will happen over the next few years. I’d also love to hear from readers about any interesting innovations you’ve seen that I haven’t mentioned.

______________

Drew Aldrich is a Senior Associate at AXA Strategic Ventures (ASV), a $250m Venture Capital firm backed by a sole LP – AXA. ASV’s US office is focused on early stage companies. He previously co-founded and led CalendarFly.com, an education technology company, and started his career in FX and analysis of esoteric structured finance products. Drew has been an active member in the NYC startup community since 2008 and actively blogs at Seeding Tech.

Drew Aldrich is a Senior Associate at AXA Strategic Ventures (ASV), a $250m Venture Capital firm backed by a sole LP – AXA. ASV’s US office is focused on early stage companies. He previously co-founded and led CalendarFly.com, an education technology company, and started his career in FX and analysis of esoteric structured finance products. Drew has been an active member in the NYC startup community since 2008 and actively blogs at Seeding Tech. ᐧ

ᐧ