As the digital world evolves, Google is taking a multi-pronged approach to maintaining its dominance in the search and ad business, which makes up the vast majority of its revenue.

Search is migrating across mediums, with users gradually moving from desktop to mobile devices and voice assistants — a shift that directly threatens Google’s moat in search and advertising.

As competition rises in the mobile and digital assistant space, and concerns over privacy and data management mount, Google has been forced to adapt.

To maintain its foothold and protect its main source of revenue, Alphabet (Google’s parent company) is positioning itself to dominate adjacent sectors — such as digital commerce, branded hardware products, and content — and attempting to integrate its services into every aspect of the digital user experience.

The company is also seeking out new streams of revenue in sectors with large addressable markets, namely on the enterprise side with cloud computing and services. Furthermore, it’s looking at industries ripe for disruption, such as transportation, logistics, and healthcare.

Unifying Alphabet’s approach across initiatives is its expertise in AI and machine learning, which the company believes will help it become an all-encompassing service for both consumers and enterprises.

In this teardown, we dive into Google’s approach to maintaining its search platform dominance, outlining the strategic investments, acquisitions, and partnerships across its top priorities moving forward.

TABLE OF CONTENTS

Alphabet’s structure and background

Google’s priorities:

- AI centricity: Embrace an AI-centric approach and solidify lead in machine learning

- Cloud: Grow share in the cloud market

- Computing: Build out a network infrastructure for computing

- Advertising: Protect advertising business from rising competition in digital — especially from Amazon

- Emerging markets: Expand in India & Southeast Asia, rebuild presence in China

Transportation & logistics: Disrupt the transportation and logistics industry

Transportation & logistics: Disrupt the transportation and logistics industry- Healthcare: Push healthcare forward through data and AI

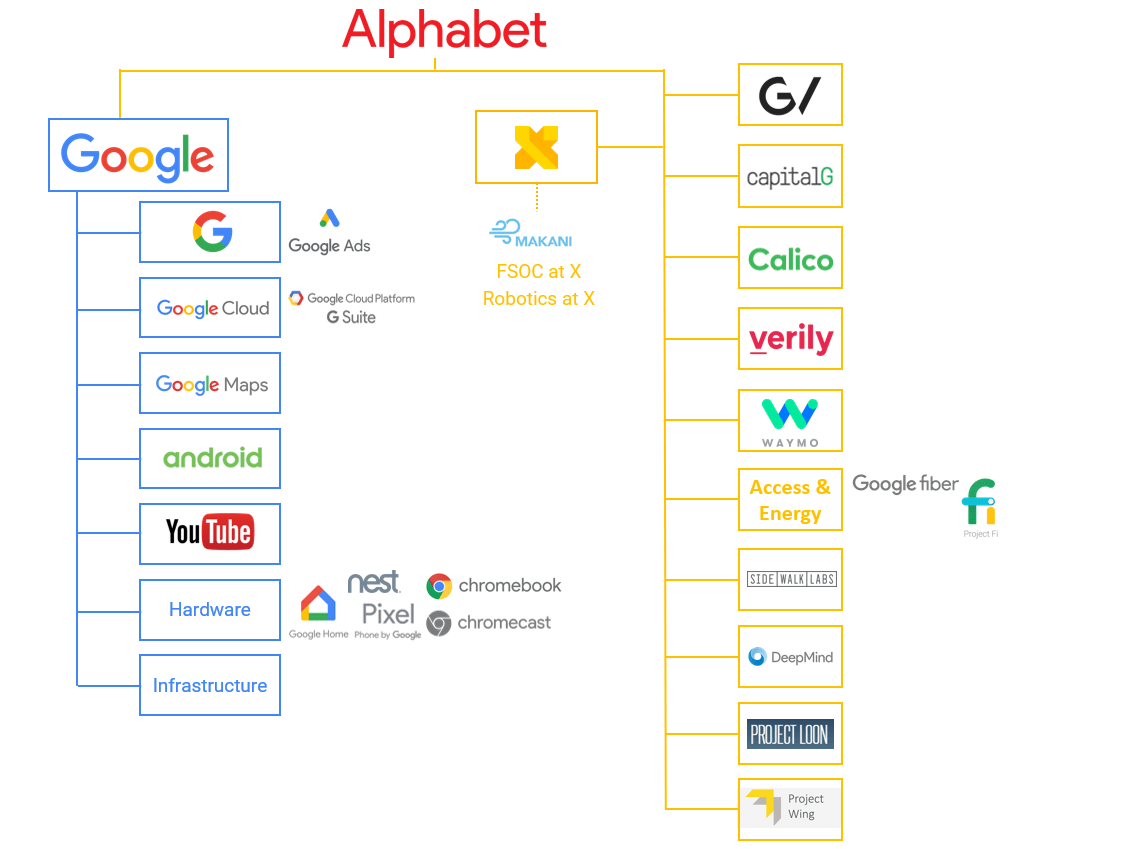

Alphabet’s structure and background

Alphabet is broken out into its core Google business and a number of other subsidiaries, which it deems “Other Bets.”

The majority of Google’s business comes from advertising revenues, which the company generates through its search engine as well as a number of other Google-affiliated and partnership websites.

Outside of search and advertising, Google generates revenue from products including cloud and enterprise, consumer hardware, mapping, and YouTube.

In addition to Google, Alphabet encompasses a host of other subsidiaries called “Other Bets.” These companies are more experimental in nature, and as a result are not material to Alphabet’s bottom line.

Google’s Other Bets include:

- GV and capitalG, two of Google’s investment vehicles

- Waymo, Google’s self-driving car initiative

- Verily and Calico, two healthcare subsidiaries

- Alphabet Access & Energy, which houses the company’s telecommunications projects and energy initiatives

- Sidewalk Labs, Alphabet’s urban innovation organization

- DeepMind, an AI research arm acquired by Google in 2014 that has the company develop neural networks

- Cybersecurity spinoff Chronicle, which focuses on security solutions for Google’s cloud business

- Project Loon, a subsidiary working to bring internet access to rural and remote areas

- Project Wing, which is developing an autonomous delivery drone service

- Google X, an R&D facility focused on “moonshot” technologies aimed at improving the world

Given that Google makes up the vast majority of Alphabet’s business, the company’s initiatives across subsidiaries have largely focused on protecting Google’s moat in search and advertising.

In recent quarters, the company has seen notable increases in traffic acquisition costs (TAC), which is the largest cost associated with Google’s main stream of revenue, ad and search. As the company faces increasing regulation (e.g. the EU’s $5B fine on Android) and an ongoing shift to mobile from desktop, TAC is expected to rise.

In addition to rising TAC, competition is growing from peers like Apple, Amazon, and Microsoft, all of which are racing to capitalize on a growing digital economy to capture data and access new streams of revenue.

As a result, Google is doing everything in its power to capitalize on potential growth areas and maintain its foothold in search and advertising.

Below, we outline the company’s main priorities, detailing the initiatives, investments, and acquisitions across its subsidiaries.

1. Embrace an AI-centric approach and solidify lead in machine learning

Artificial intelligence is critical to Alphabet’s long-term outlook. AI is the thread that runs through search & advertising, cloud, autonomous driving, healthcare, and a host of the company’s Other Bets, as we’ll outline futher below.

WHAT it’s DOING now

In a keynote presentation to launch Google’s new high-end Pixel smartphones in October 2016, CEO Sundar Pichai highlighted the importance of artificial intelligence to the tech landscape moving forward, explaining, “It is clear to me we are evolving from a mobile-first to an AI-first world.”

Since then, AI has become the company’s focus across its investments, acquisitions, and internal spending.

Investments

Google has launched two funds dedicated solely to AI: Gradient Ventures and the Google Assistant Investment Program.

Gradient Ventures was launched in July 2017. Unlike GV and capitalG, which run separately from Google under the Alphabet corporate framework, Gradient Ventures is accounted for on Google’s balance sheet. That said, the fund plans to break off from the main company once it ramps up its investment pace.

So far, Gradient has only invested in early-stage deals, primarily focusing on the US — though a recent investment was in Canada-based Benchsci, a medical sciences startup using AI to accelerate biomedical discoveries.

Google has also launched a fund to build out its capabilities for Google Assistant, Google’s virtual assistant that uses natural language processing to take voice commands from users and search the internet, schedule events, set alarms, among a host of other tasks. Launched in May, the Google Assistant Investment Program is focused specifically on early-stage startups working with Google’s virtual assistant.

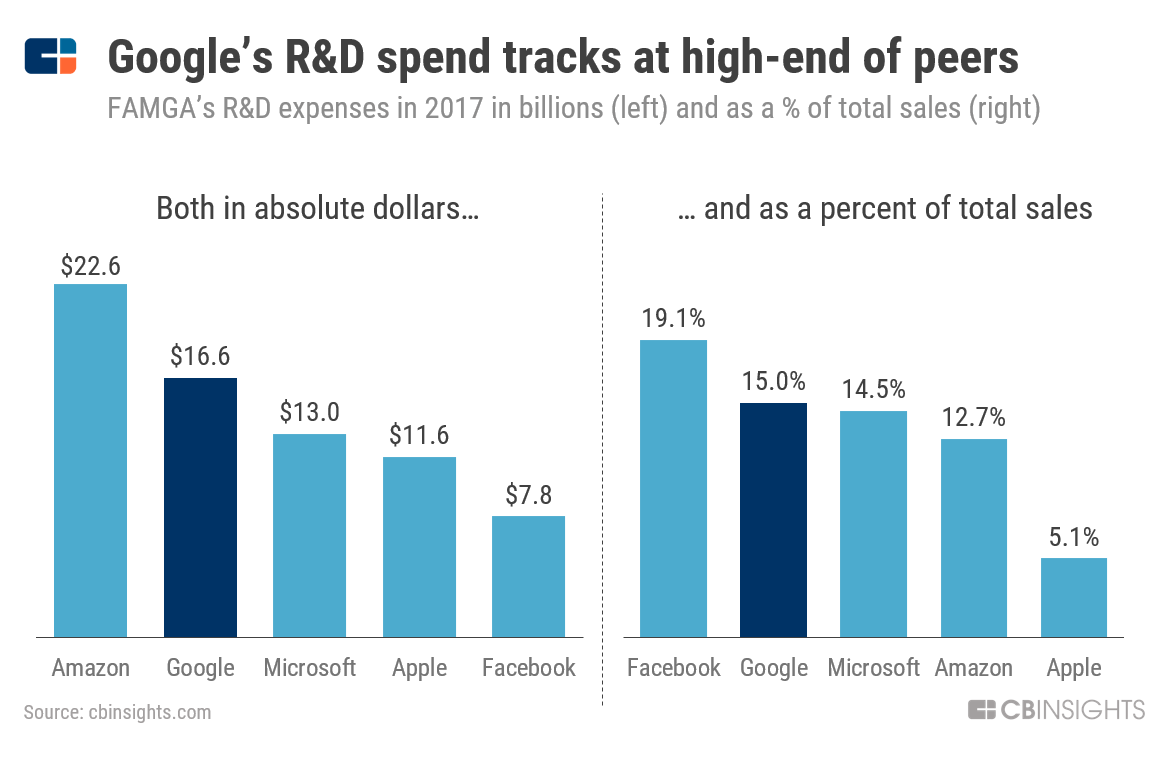

Google is also investing internally in its machine learning capabilities by ramping up its R&D spend, which it largely dedicates to its main areas of strategic focus (such as search and machine learning). In 2017, Google tracked at the high-end of FAMGA in terms of R&D spend in absolute dollars as well as relative to sales.

The company has also ramped up its capex spend, which largely funds its computing infrastructure. (We outline this in further detail below.)

Acquisitions

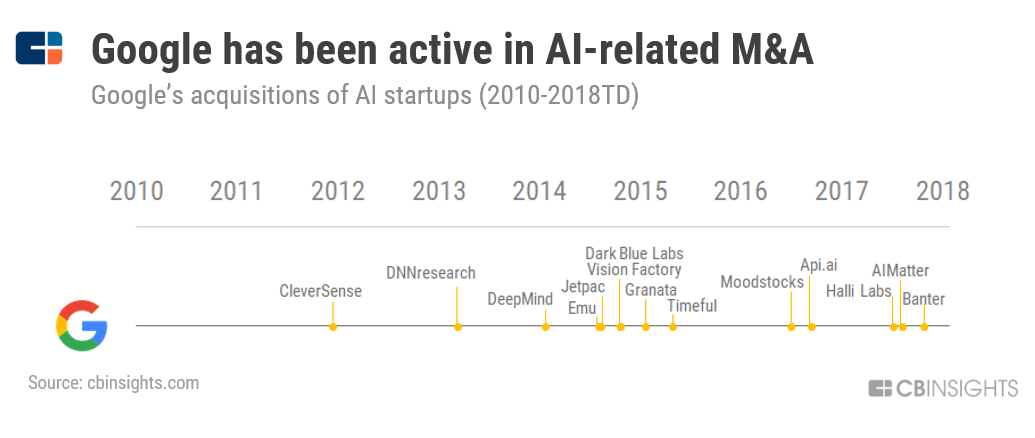

In addition to investing through its new investment vehicles and more established funds, Google has also been actively acquiring AI startups for the past few years.

One of the company’s initial forays into AI and machine learning was its $600M acquisition of AI startup DeepMind in January 2014. DeepMind currently operates as a subsidiary of Alphabet, and has been a pioneer in the machine learning space, with its program beating a human world champion in the board game “Go.”

More recently, the company acquired Halli Labs, an India-based AI startup focused on deep learning and machine learning systems, and AIMatter, a computer vision company using a neural network-based AI platform to process images. The company also acquired Banter in November 2017 to build out its natural language processing capabilities for enterprise cloud services like Google Hangouts.

Product launches

Google has heavily emphasized the importance of building a superior digital assistant. The company is facing rising competition from Amazon and Apple, both of whom have launched their own virtual assistants. This poses a significant threat to Google’s core business, as every voice-based search that consumers perform using Alexa or Siri takes business away from Google’s search platform.

In terms of scaling its digital assistant, Google CEO Sundar Pichai has said that the company is working with “every major device brand” in the US to cover a wide range of products, from dishwashers to security systems.

![]()

Google’s first smart home hub with a screen, manufactured by Lenovo.

Google is also buildling out its own hardware manufacturing capabilities for its in-house products, known as the Made by Google line. This includes the Pixel smartphone, the Chromebook laptop, and the Google Home smart home device.

A number of Google’s recent investments and acquisitions have been focused on building out its hardware capabilities, most notably its $1.1B acquisition of hardware manufacturer HTC’s smartphone division in September 2017. With the deal, Google gained access to HTC’s hardware engineers and also established a manufacturing presence in Taiwan.

Patents

The main engine for Google’s internal research on AI and machine learning is Google AI. Formerly known as Google Research, the project was recently re-branded to reflect the company’s newfound focus on AI.

Within Google AI sits the Google Brain team, which has led the charge in developing TensorFlow, Google’s open-source software library. The team also improves core capabilities from translation to voice search.

Google Brain works closely with a number of Alphabet’s subsidiaries, including autonomous driving division Waymo, where it has helped apply deep neural nets to vehicles’ pedestrian detection system. The team has also made inroads in the energy space, helping Google realize cost and environmental savings at its power-hungry data centers to improve power usage efficiency by 15%.

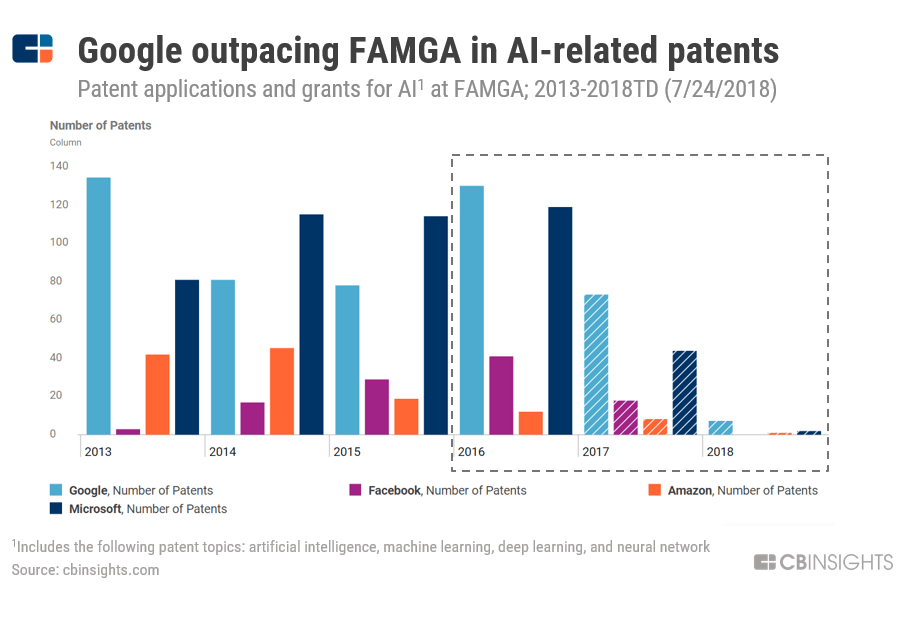

The team has been highly-focused on AI and machine learning, evidenced by a jump in AI-related patent activity starting in 2016.

Note: Patterned columns may be incomplete due to the delay between patent filing and publication.

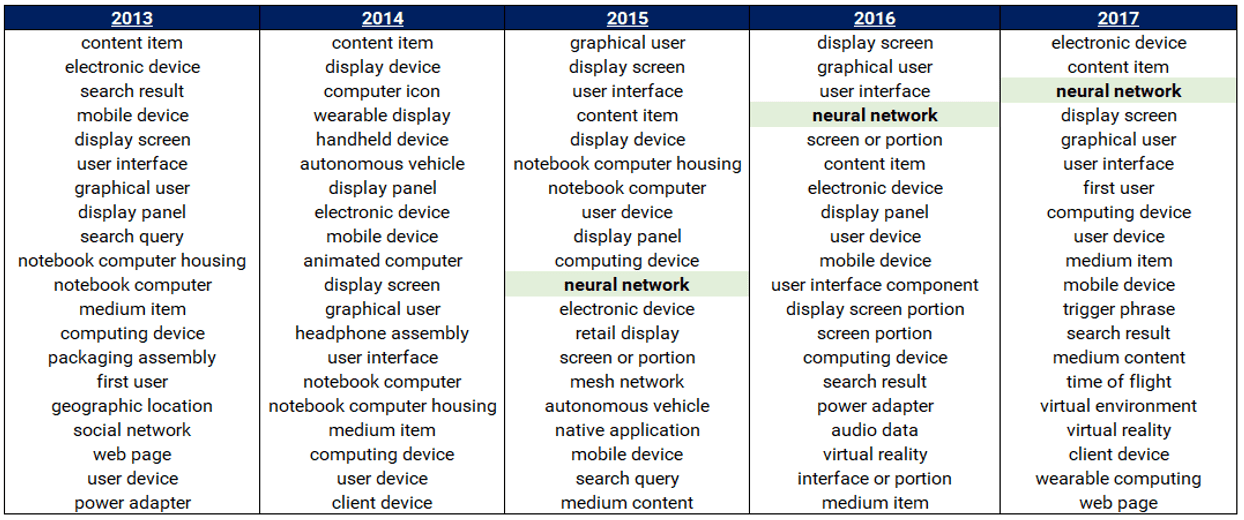

Google is also focused on building out its deep learning capabilities, which is more complex than traditional machine learning in that it generates predictions using an artificial neural network inspired by the human brain. Unlike machine learning, deep learning algorithms do not require adjustments from engineers and should be able to determine on their own if predictions are accurate or not.

Google’s emerging focus on deep learning can be seen in the company’s top patent keywords (pictured below). “Neural network” was first mentioned in 2015 and has since climbed to become one of the top 3 most frequently mentioned terms.

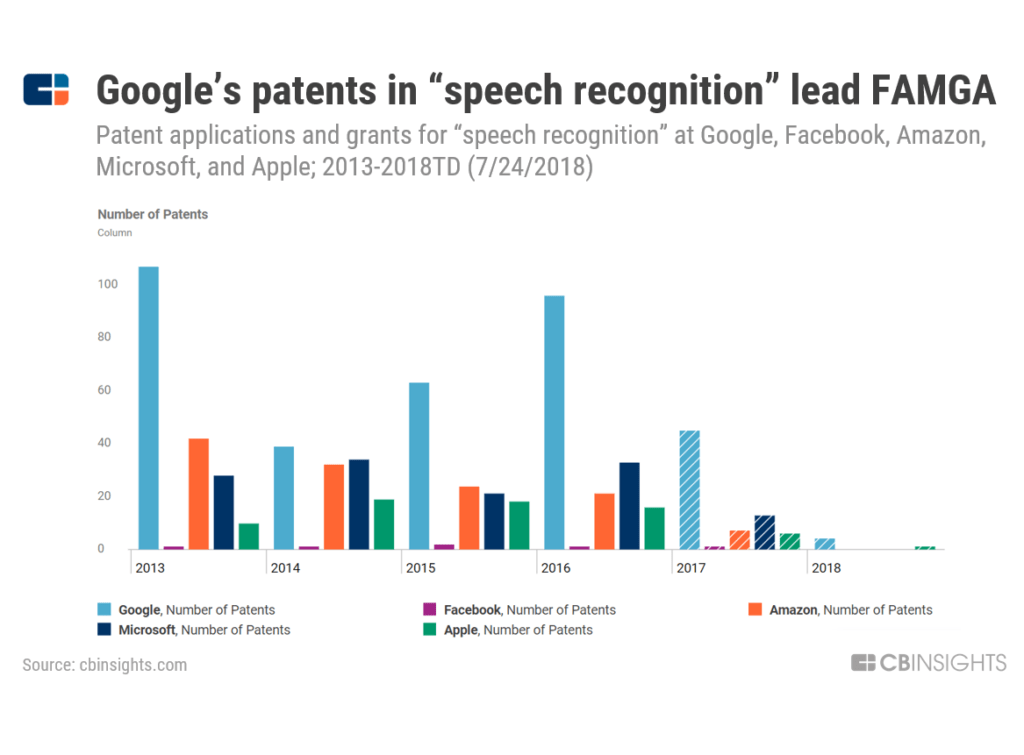

Google has also focused heavily on speech recognition and natural language processing. The company’s IP activity around voice has outpaced FAMGA historically.

Note: Patterned columns may be incomplete due to the delay between patent filing and publication.

In 2016, Google’s patent activity related to speech recognition reaccelerated, reflecting the company’s mission to dominate the digital assistant market.

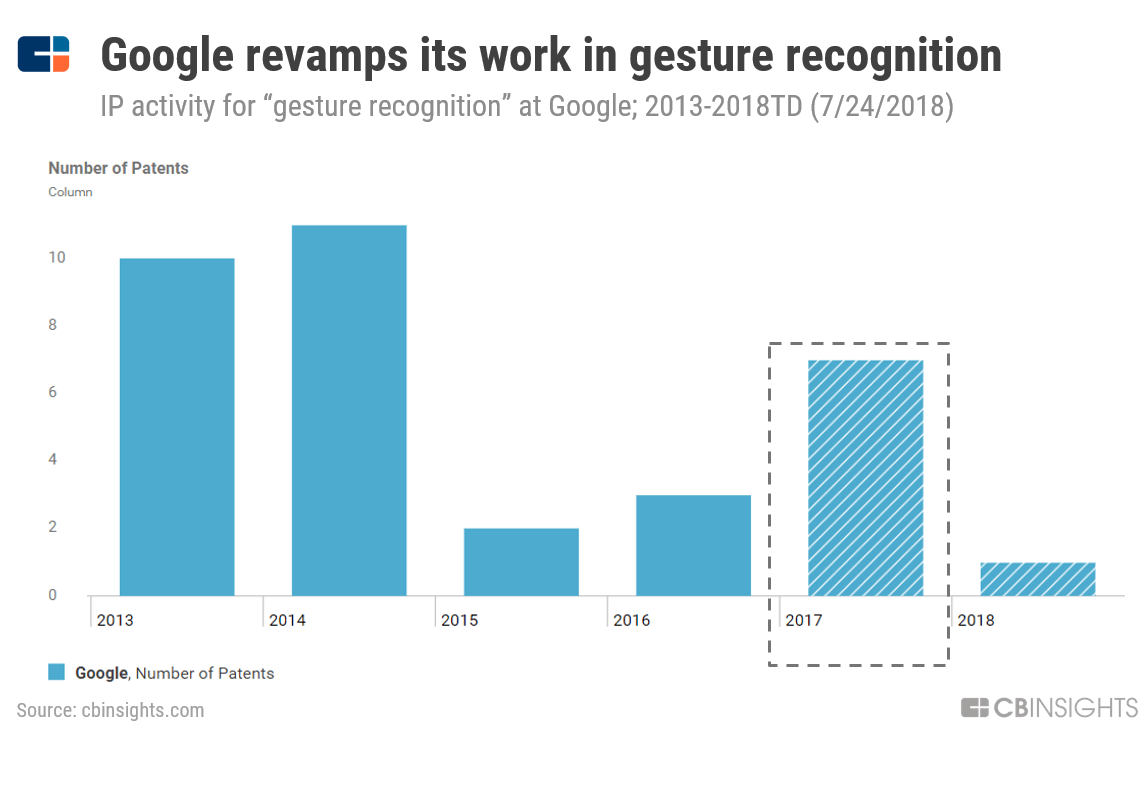

Beyond speech recognition, another area related to digital assistants is gesture recognition. In recent months, Google has upped its IP activity in the gesture recognition field.

Note: Patterned columns may be incomplete due to the delay between patent filing and publication.

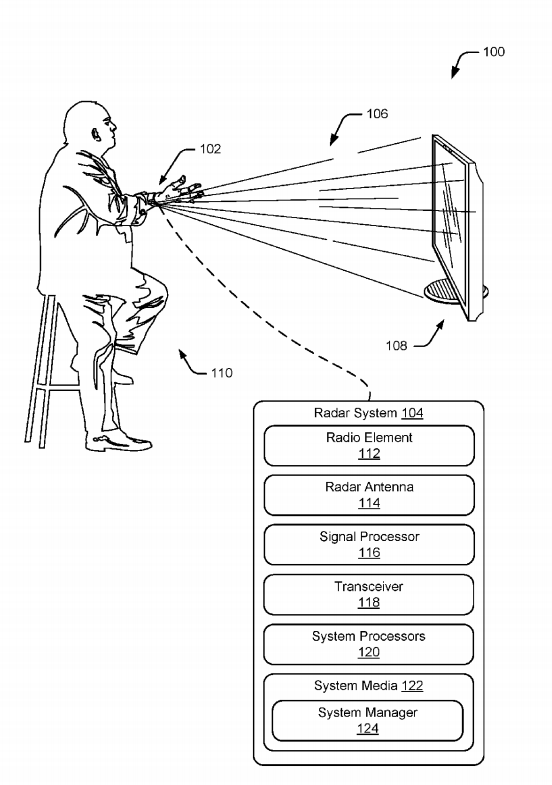

Google’s patents offer clues as to how the company plans to integrate voice and gesture recognition into its products in the future.

In October 2017, Google filed a patent for “radar-based gesture sensing and data transmission.” The technology would allow users to control a suite of devices using gestures, rather than just voice or other control devices (like a TV remote or buttons on a microwave).

This patent hints at Google’s vision for an automated home that still relies on instructions from a user.

WHERE it’s going next

Google’s recent investments and activity suggest that the company is prioritizing deep learning and natural language processing so that it can more effectively process and manage growing amounts of information from both consumers and enterprises.

As CEO Sundar Pichai said at the Google I/O conference, Google is rethinking “all” of its products for an AI-driven future.

With AI as the priority, the company is focused on developing sophisticated machine learning capabilities through both outside investments and in-house development.

News

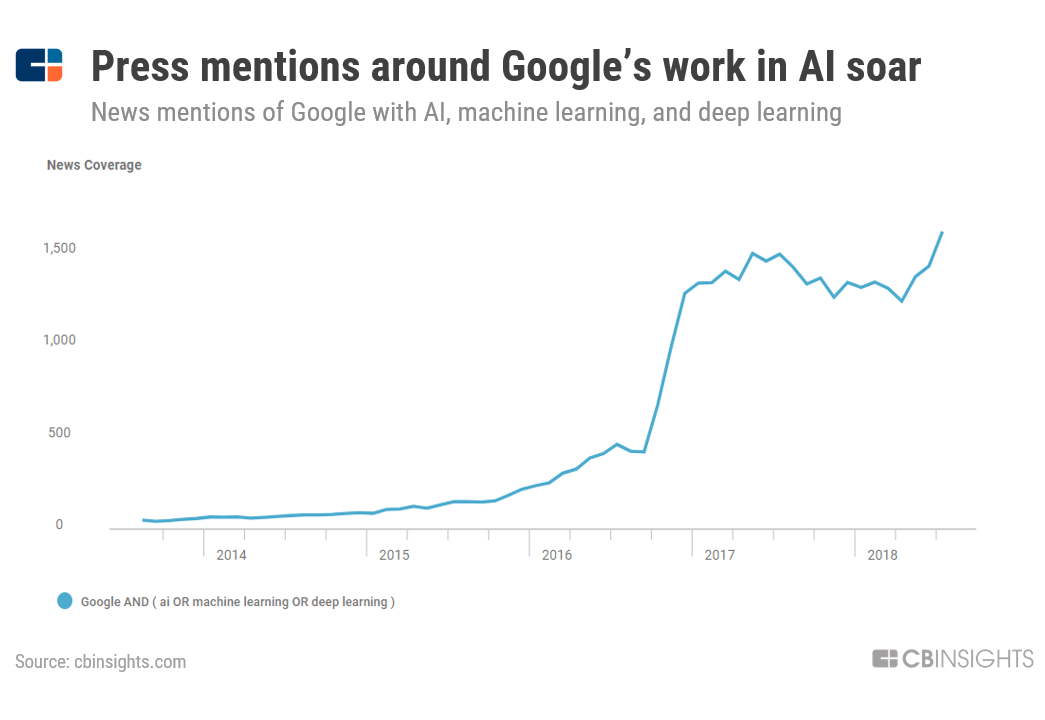

Based on the CB Insights Trends tool, which aggregates news mentions across press sources, mentions of Google and AI, machine learning, or deep learning have picked up substantially in recent months.

On the digital assistant front, Google is making notable headway to differentiate its assistant from Amazon’s Alexa and Apple’s Siri.

Recently, the Google Assistant has been more top-of-mind than both Alexa and Siri — news mentions of the Google Assistant outpaced mentions of both virtual assistants for the first time in its history.

Earnings transcripts

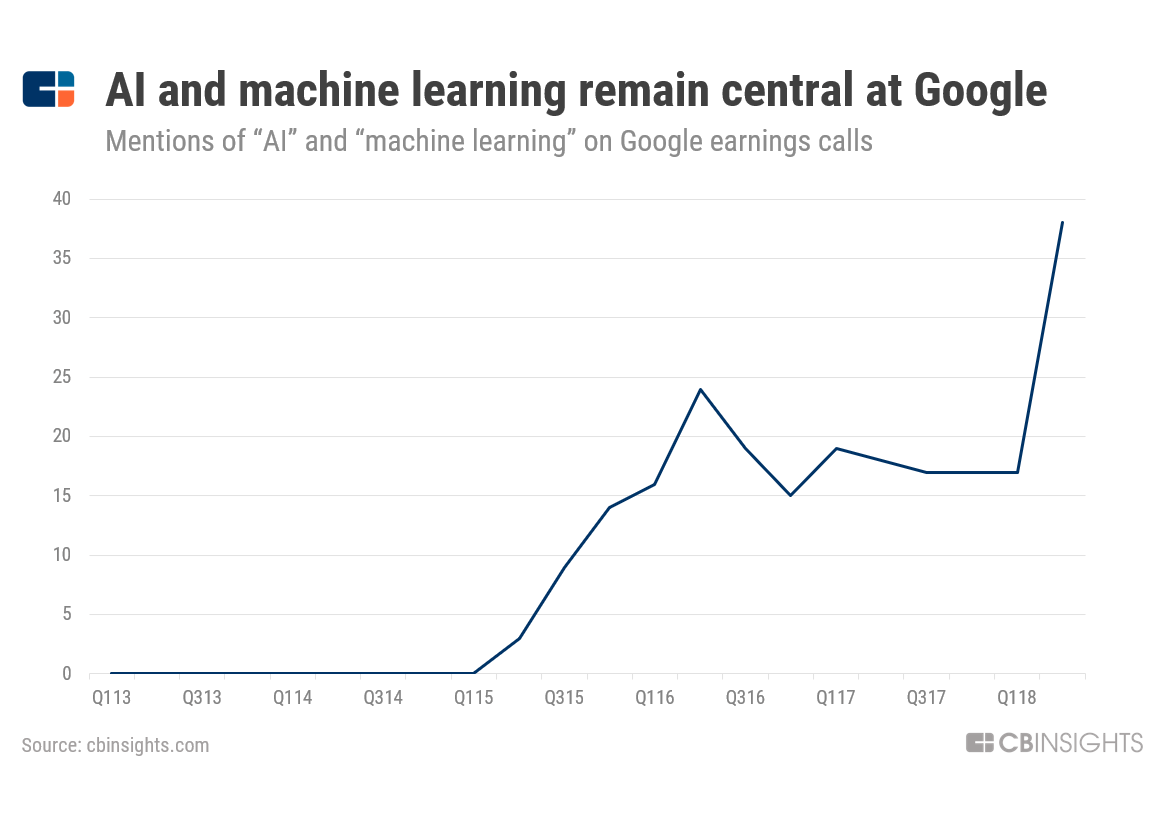

Though artificial intelligence has been a key focus for over a year, Google’s mentions of “AI” and “machine learning” on earnings calls reached a new peak in Q2’18.

Ultimately, Google wants to “help users get things done” through a combination of search and assistant. In Q4’17, Pichai noted that the company has room for improvement on the user experience end:

“…at a high level the next big evolution we are doing as part of mobile search and Assistant is to actually help users complete actions, to help get things done. And it’s really hard to do at scale, and that’s the work we are doing.”

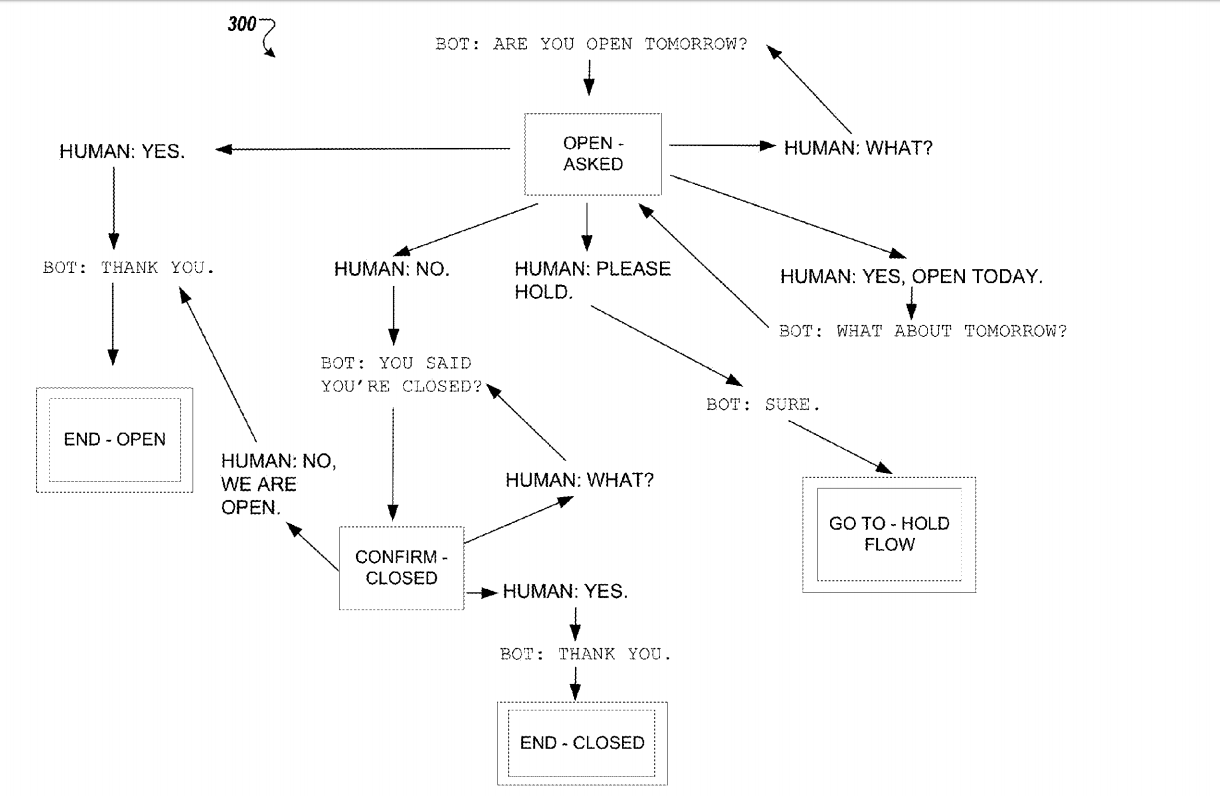

At its I/O conference in May, the company outlined a future capability for the Assistant: a voice system that can carry out phone calls on a user’s behalf.

Called Duplex, the technology is the first of its kind among even the most advanced digital assistants and ushers in a new stage in the race for voice and AI supremacy.

The below image — taken from Google’s 2017 patent application for similar technology — outlines a simplified version of one of these conversations.

Google’s vision to dominate the smart home market and own the entire stack of hardware devices ties in closely with the digital assistant. The company has focused on its presence in hardware to build out its devices end-to-end, in part to relieve rising costs from third-party hardware manufacturers and also for more seamless integration between its software and hardware.

The decision to bring its Nest business back under Google’s hardware division signals Google’s interest in integrating all its products with a simple assistant, which would provide the company with more channels to advertise and provide information to consumers.

Ultimately, the more Google is able to scale its virtual assistant technology across its suite of products — in everything from mobile devices to the Google Home to other connected personal devices — the better the foothold it will gain in the search and advertising world.

WHY is this a priority?

AI substantially impacts just about all of Alphabet’s businesses and stands to upend a number of large industries. By differentiating itself across its businesses through machine learning, Alphabet can better solidify its dominance in search and advertising.

Market sizings

The market for AI and machine learning is hard to size, given that the technology is ubiquitous and has the potential to tackle inefficiencies across a wide array of industries.

The digital assistants market (which is simpler to size) is expected to reach $12B by 2024. Additionally, Google’s foray into smart home devices could tap into an estimated $122B market by 2022.

Building out the most sophisticated digital assistant helps strengthen Google’s dominance as a search platform provider. As a result, search and the Google Assistant — projects that Pichai said sit at the “heart” of Google’s business — are intricately tied together in Google’s future strategy.

2. Grow share in the cloud market

Google currently ranks third among cloud providers, after Amazon and Microsoft. However, the company has built out its presence in the space through a number of investments, acquisitions, and internal efforts. It has also launched multiple initiatives to better compete with other tech giants.

WHAT IT’S DOING now

Though it trails Amazon and Microsoft in the cloud space, Google has made notable inroads and is currently growing the fastest of the three services.

On its Q4’17 earnings call, the company announced that its cloud business is now bringing in $1B per quarter. The number of cloud deals worth $1M+ that Google has sold more than tripled between 2016 and 2017, and G Suite, Google’s set of cloud-based productivity applications, had over 4 million paying customers.

Investments

Google has ramped up internal investments for its cloud business.

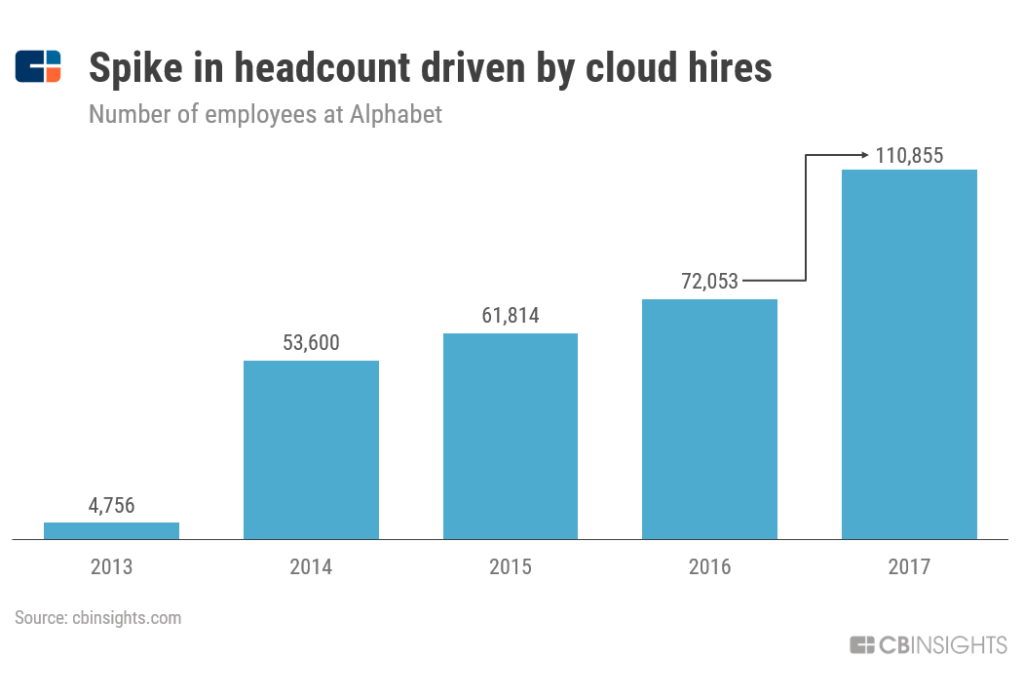

For four quarters in a row, the company has attributed its headcount increases to hires for cloud, including both engineers and go-to-market strategists.

CEO Pichai has also attributed rising capex spend — which includes the cost of data centers, machinery, real estate, and information technology — to building out the cloud business. As he detailed on the Q1’17 earnings call:

“On the Cloud stuff, in Q1, our largest growth in head count and CapEx was in Cloud. The heavy lifting, I would say, is around how we meet enterprises in the market. We have reorganized so we have one face to the customer. So it’s not just sales reps. We’ve been thoughtful about how we have built out the entire go-to-market organization.”

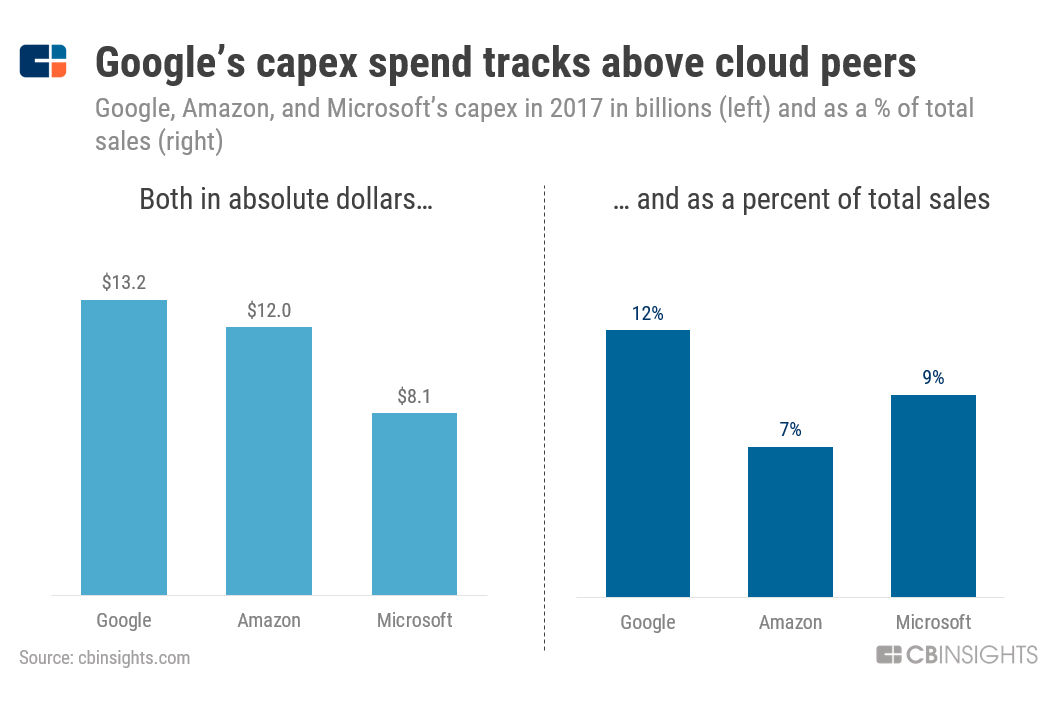

This heightened spending has driven the company’s capex above both of its cloud rivals, Amazon and Microsoft.

Google has made a few investments in cloud startups through its investment funds. Most recently, in March 2017, it participated in a $14M Series E round to cloud storage startup Avere Systems. In January 2018, Avere was acquired by Microsoft.

Acquisitions

On the M&A front, cloud is Google’s primary focus, as it veers away from its historical preference for moonshots (e.g. AR/VR, space exploration). As Alphabet CFO Ruth Porat noted in an interview at Recode’s Code Conference:

“The acquisitions that we’ve talked about really in particular fill in holes in cloud, and that’s been really valuable.”

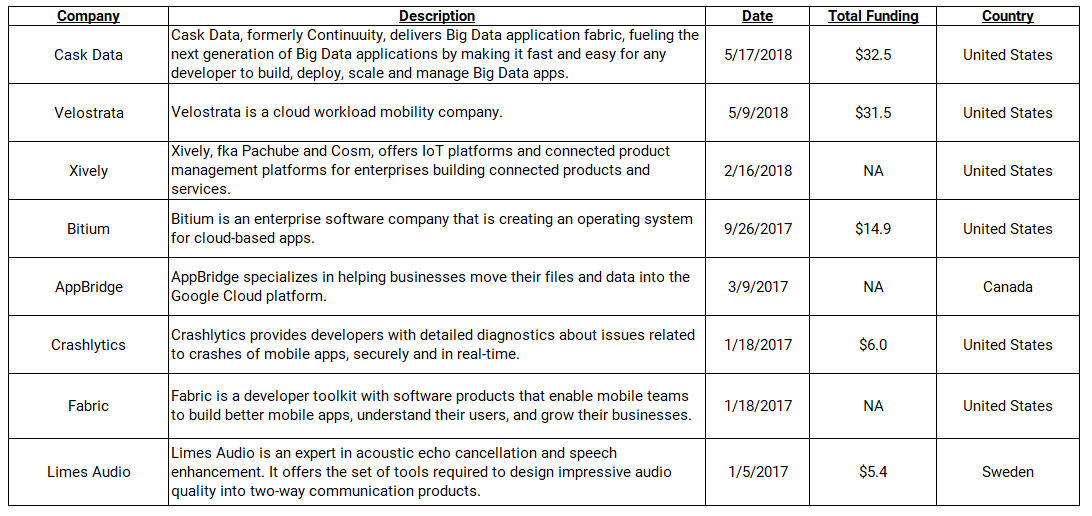

In 2018, the company has already made several acquisitions in the cloud space, including Cask Data and Velostrata in Q2’18 and Xively in Q1’18. Its other recent acquisitions in the cloud space include the following:

Product launches

Google initially built out its enterprise business by focusing on SMEs, consumers, and students, but it failed to gain traction at larger, more established enterprises.

Now, Google sees the most opportunity for its cloud business on the enterprise side. The company brought in VMWare’s Diane Greene to run its enterprise offering, which has given birth to a number of enterprise-focused products, including G Suite.

As its built out its enterprise business, the company has landed several reputable partnerships with major corporations, including Cisco, Salesforce, and SAP, and is focused on strengthening its capabilities not just in cloud services but also in its go-to-market strategy.

As CEO Pichai noted on the company’s Q4’17 earnings call:

“These collaborations span our entire company, from engineering integration to marketing programs to joint sales, and they cover Google Cloud Platform, G Suite, and Google Analytics.”

To gain further ground in the enterprise space, Google launched a number of new products and services at its Cloud Next conference this July.

One of the most celebrated releases was Google Cloud Services, a family of services that allows users to extend the Google Cloud Platform to in-house servers or edge devices, catering to businesses that prefer to use a blend of public and private cloud services.

Google also announced a specialized chip called the Edge TPU, which can carry out machine learning processes in IoT devices. The chip is intended for use to manage larger-scale workloads.

Google’s Edge TPU

Cloud-supported blockchain applications have historically been a less-explored area for Google. However, at its cloud conference the company announced the planned integration of blockchain technology into its cloud platform, through a partnership with blockchain startups Digital Asset and BlockApps.

WHERE IT’S GOING next

News

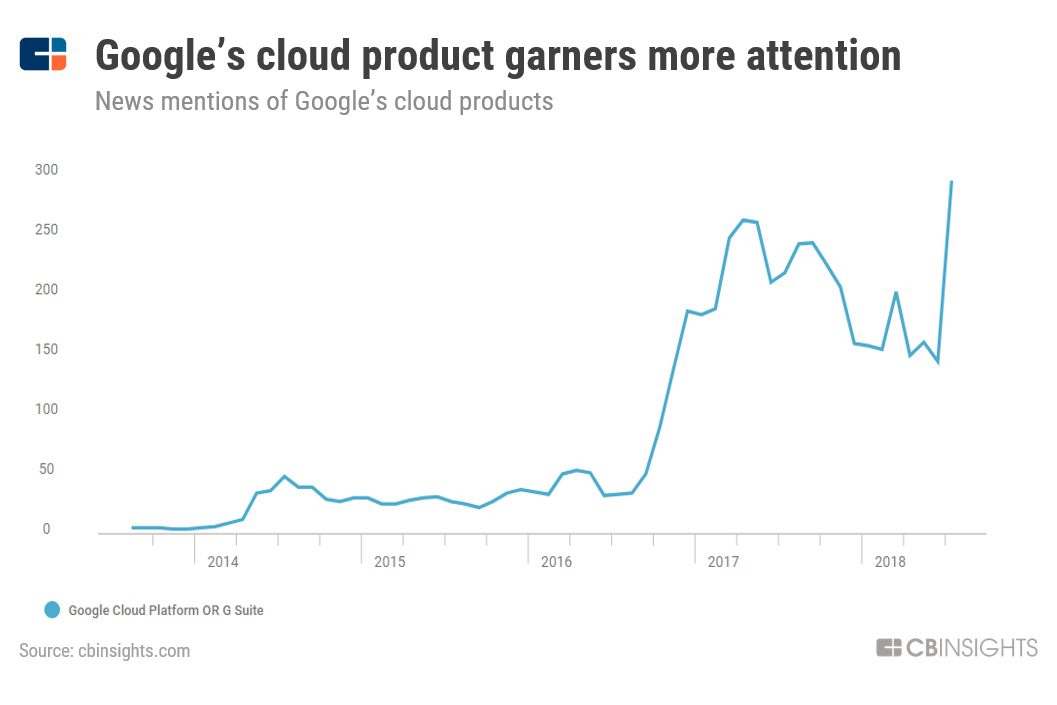

Google has successfully established itself as a major player in the cloud space, with its cloud products increasingly gaining media mentions, despite still lagging Amazon and Microsoft.

Earnings transcripts

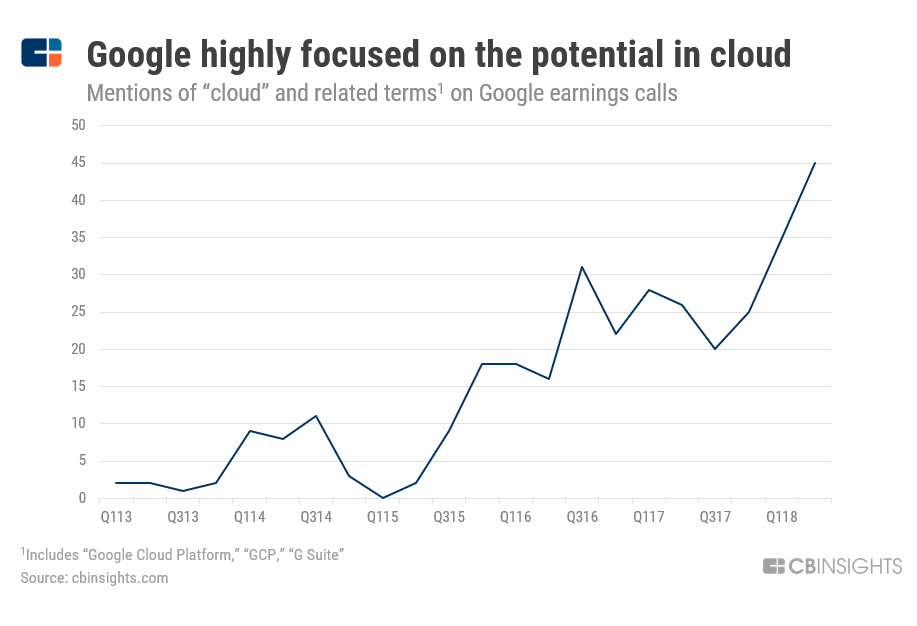

Even though cloud has been top-of-mind for Google for several years now, mentions of cloud and cloud-related products reached a new peak in Q2’18, suggesting that the company sees increasing opportunity in the space.

Google sees a number of opportunities to leverage its expertise across other verticals (like content and digital commerce) in order to get its foot in the door with enterprises facing a growing need for cloud services.

The company also sees an opportunity for its cloud business within regulated industries like financial services and healthcare. When asked about the company’s approach to heavily regulated industries, CEO Pichai said:

“That’s where a lot of our investments have gone, getting certifications needed, depending on the industry and building the features that you need… And that’s clearly starting to have an impact, both on GCP, but as well as G Suite. We definitely are going to continue to build out our capabilities. And we’ll be going after the opportunities in these areas very seriously.”

Cybersecurity, which is critical for the cloud business, has become another area of focus for Google and other tech giants. Google spun off its cybersecurity arm, Chronicle, from Google X in January 2018 to work on detecting threats to enterprise security faster that current systems. Ultimately, the spin off is intended to create what Google X chief Astro Teller calls a “digital immune system.”

WHY IS THIS A PRIORITY?

An increasing number of businesses are generating more information, and as a result need incremental computing and processing power to make sense of it.

All of this will require more complex computing and additional computing infrastructure, which Google believes it can handle through its machine learning capabilities.

Despite trailing behind Amazon and Microsoft in the cloud space, Google has an opportunity to capture some business from these competitors as customers seek expertise in machine learning, an area where Google remains differentiated.

Market sizing

Google’s presence in the cloud industry allows it to tap into a number of growing markets in the cloud space, including cloud computing, which is expected to reach $513B by 2022, and cloud storage, which is expected to reach $90B by 2022.

3. Build out a network infrastructure for computing

What it’s doing now

Investments

Google is heavily invested in developing a network infrastructure to handle higher levels of computing. The company has cited that one of the main drivers of its capital expenditures is building out compute capacity, as more complicated machine learning capabilities increasingly require more processing power.

As Ruth Porat explained on the Q2’18 earnings call:

“We’re focused on capex as a lens into the outlook for growth for additional compute capacity, which has a number of growth drivers, including supporting growth in our search and ads business as well as newer businesses.”

On the network infrastructure front, Google has built out a data center network to support its growing cloud business. The company currently operates 15 data centers across the globe (8 in the US, 4 in Europe, 2 in Asia, and 1 in South America) which house its compute, storage, and data replication services.

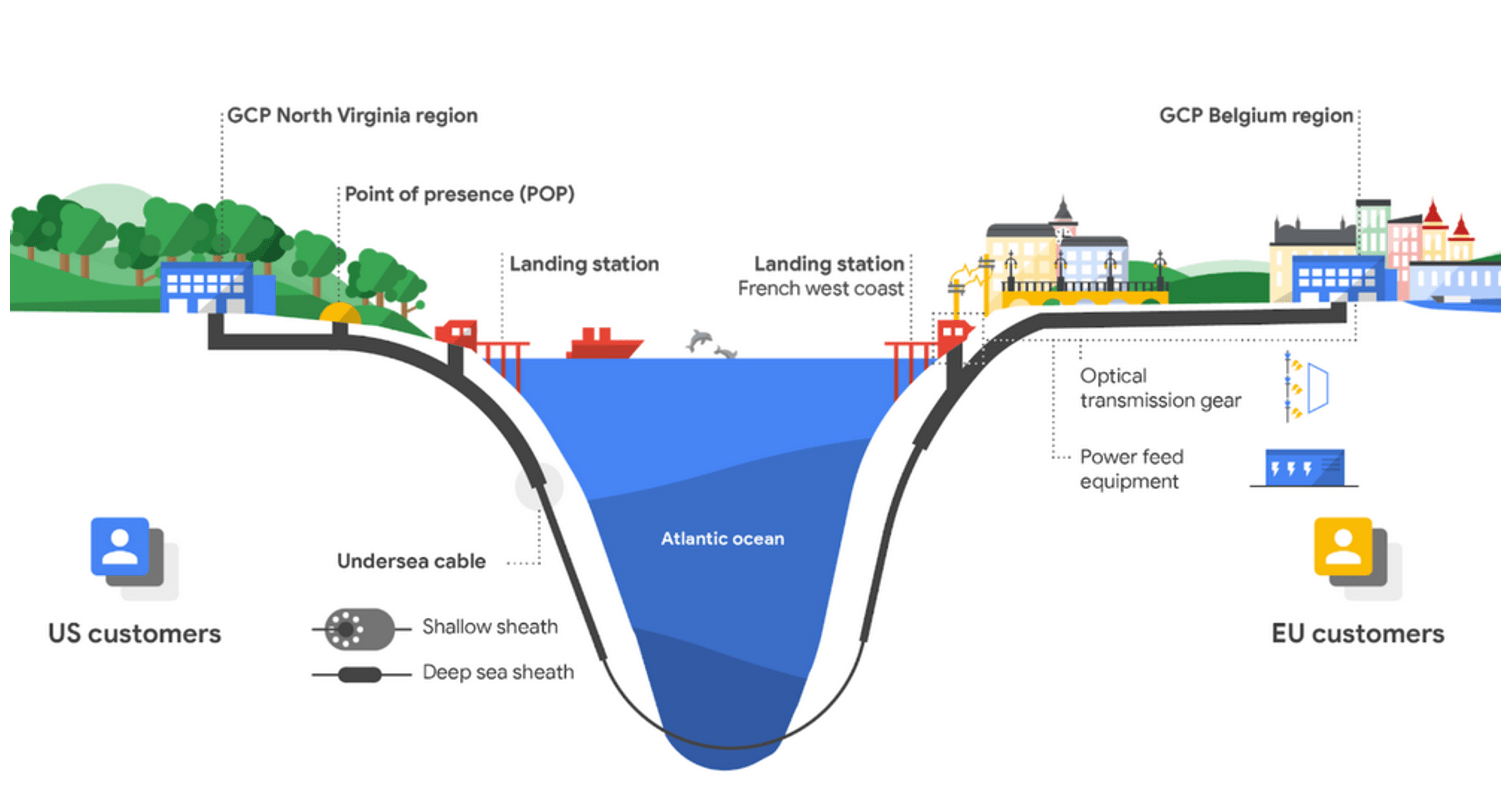

Additionally, Google has invested heavily in a number of subsea cable projects to support its computing capabilities. In July, the company announced a private subsea cable project that will cross the Atlantic Ocean. Dubbed the Durant cable, the system will be the first private trans-Atlantic cable built by a non-telecom company. The cable is intended to increase network capacity across the internet and also support the growth of Google Cloud.

WHERE IT’S GOING next

Looking ahead, it’s clear that Google aims to pioneer the most advanced computing technology, which at the moment seems to be quantum computing.

Quantum computing provides substantially more processing power than a traditional computer, processing more information and at a faster rate. As co-founder Sergey Brin outlined in the company’s 2017 Founder’s Letter:

“For a specialized class of problems, quantum computers can solve them exponentially faster. For instance, if we are successful with our 72 qubit prototype, it would take millions of conventional computers to be able to emulate it.”

As a result, Google is investing substantially in quantum computing, and has come to be seen as one of the leaders in the space, along with Intel and IBM.

Google’s Quantum team sits under Google AI. The team is working on advancing quantum computing by developing quantum processors and novel quantum algorithms.

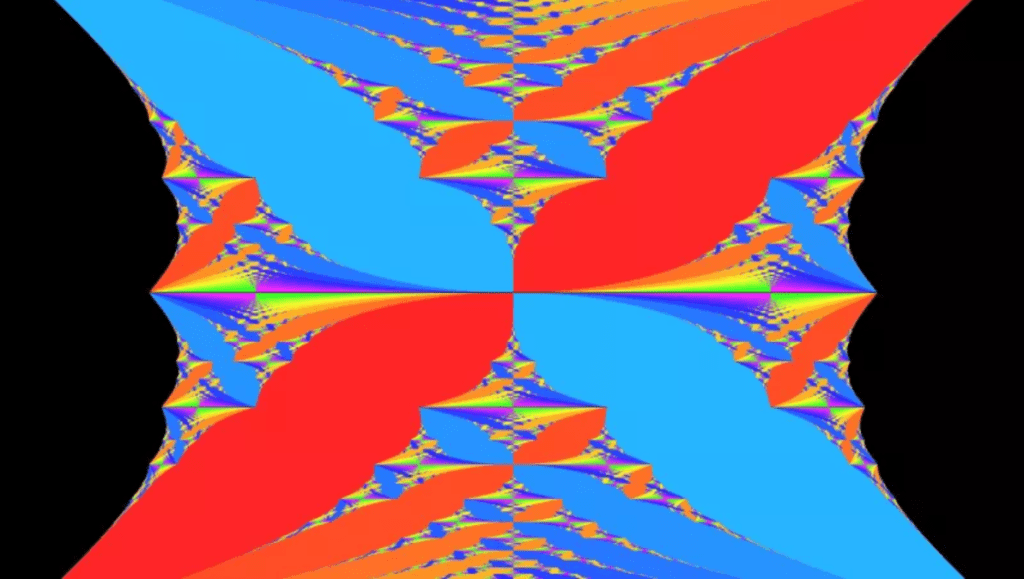

In July, the Quantum team launched an open source software platform called Cirq. The platform allows users to run quantum algorithms on Google’s simulator. The below image, called Hofstadter’s butterfly, shows how electrons would behave in such a simulated magnetic field.

Quantum computers use qubits, which are more sophisticated than standard digital bits that represent either 1 or 0. Qubits, however, can be in both states at once (1 and 0) thanks to a phenomenon known as superposition.

Google has also developed hardware that can support quantum computing. For example, its Bristlecone chip currently holds the record number of “qubits.”

Ultimately, quantum computing can be used to run a wide variety of machines more efficiently.

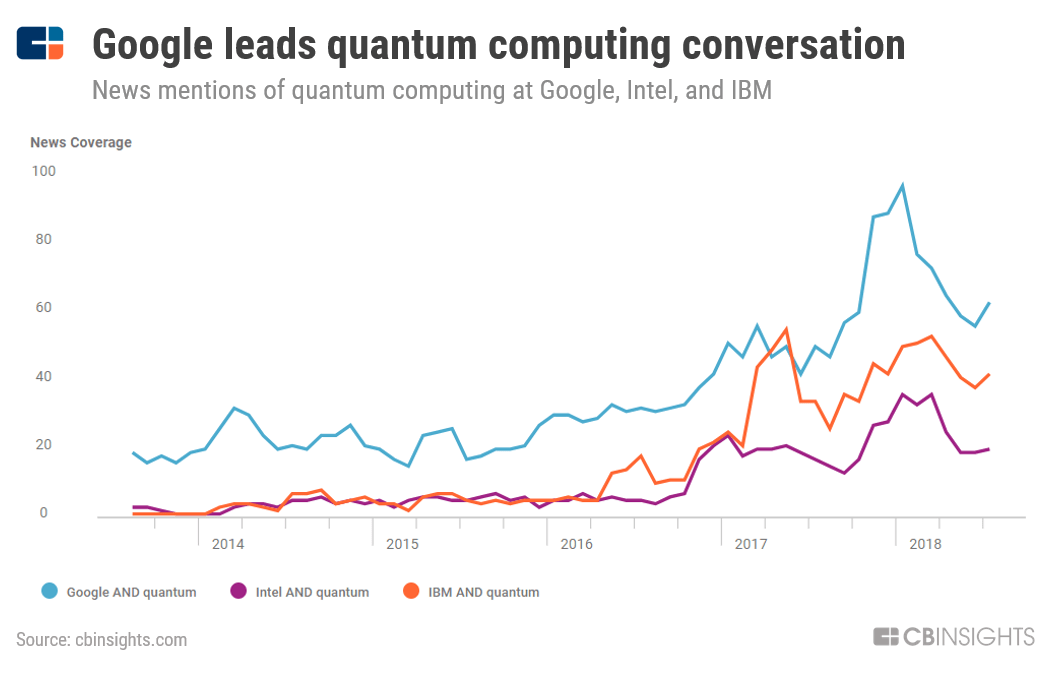

News

Media mentions of Google’s quantum computing efforts have recently come to exceed mentions of Intel’s and IBM’s efforts in the space.

Earnings transcripts

On Google’s company earnings calls, quantum computing has yet to enter the conversation. That said, senior management prioritizes computing hardware, namely Google’s tensor processing unit (the TPU), which has been built specifically for machine learning and tailored for TensorFlow, its open source machine learning software platform. In February 2018, the company announced that it was making TPUs available in beta on the Google Cloud Platform.

According to Google, the TPU is faster and substantially more energy efficient than contemporary processing chips such as CPUs (central processing units) and GPUs (graphic processing units).

WHY IS THIS A PRIORITY?

As Google increases its capabilities in machine learning and cloud, it will need to build out the infrastructure to support it, such as fiber-optic cables. According to the company’s SVP for technical infrastructure, Urs Hölzle, Google needs to double its transmission capacity each year to maintain its core businesses.

Fiber-optic cables have traditionally carried telephone traffic, but lately, content and cloud computing flows are dominating traffic flow, making up 77% of data traffic across the Atlantic Ocean and 60% across the Pacific Ocean in 2017. As a result, Google is investing in submarine fiber-optic cables (as mentioned above), most notably to connect to areas with growing internet usage, such as China.

In addition to network infrastructure, the company also must build out the computing capabilities of its own hardware so that it can own the computing stack from end-to-end.

4. Protect advertising business from rising competition in digital — especially from Amazon

What it’s doing now

With Amazon’s recent rise to the top of e-commerce, Google has lost a substantial amount of its product advertising volume, which makes up roughly 60% of the company’s ad clicks. Additionally, both Amazon and Apple have spent billions on content and music services to make their media/app platforms stickier, posing a direct threat to Google’s ability to dominate its advertising business across platforms.

Now, Google is fighting back, making a notable push in the digital commerce and content arena. The company’s efforts here reflect its attempts to take back its leadership in product search and prevent share loss in other advertising channels.

Product launches

One examples of Google’s recent attempts to reclaim its territory in product search includes its March 2018 launch of Shopping Actions, a tool that integrates the retail experience across Google’s platforms (including mobile, desktop, and voice-powered devices). Early tests suggest that the project is increasing online shopping cart sizes by as much as 30%.

In 2017, Google partnered with a number of major retailers, including Walmart, Target, and Costco, to bolster its delivery platform, Google Express. The platform allows users to shop across a number of retailers with free delivery over a certain threshold.

Google has also launched several services in the content space to make its broader platform stickier. Through its Google Play platform, users can access the Android app store, as well as music, magazines, books, movies, and television programs — competing with Amazon’s multitude of Prime services aimed at content consumption and Apple’s suite of content offerings.

Google has seen substantial growth in its YouTube business, through which it has started to offer paid channel memberships. It can also tap into revenue from merchandise shelves on YouTube channels and other endorsement opportunities.

Parallel to its efforts to build out content delivery, Google has launched a number of initiatives related to improving internet connectivity (as discussed above).

Google Fiber was the company’s initial foray into providing broadband internet to the masses. The project offered faster internet access to businesses and residents of a few select cities throughout the US. However, given how capital intensive it was to scale its fiber-optic infrastructure, the company eventually stalled plans to expand.

While Google’s telecom division, known as Alphabet Access, has struggled to scale and gain market share from major incumbents like AT&T and Comcast, Google’s attempts to disrupt the network connectivity space have spurred innovation from incumbents, which has allowed Google to broaden content delivery capabilities and reach.

WHERE IT’S GOING next

Earnings transcripts

Capturing digital commerce is critical to Google’s strategy moving forward, as it allows the company to recapture a portion of the product searches it has lost to Amazon while also providing another valuable avenue for collecting consumer data.

In Q4’17, CEO Pichai spoke to the importance of building out Google’s presence in digital commerce:

“E-commerce is evolving a lot and we continue to invest there. Google shopping is doing well. And we work hard to make sure we bring the best experience possible, which is why we partner with companies like Walmart for example to make it easier to buy products. Consumer behavior is changing but we are comfortable given the breadth of how we do things and how we are focused on user experience there.”

Digital commerce is also inherently tied to Google’s cloud business. The more retailers that Google partners with on the digital commerce front, the more opportunity it has to extend its expertise in enterprise cloud services. Pichai touched on this in the Q2’18 call:

“On the commerce front, obviously, it’s a natural sector I think for us to drive partnerships. We already have deep advertising relationships with many of these providers, increasingly. Shopping is an area where we are beginning to work together. And finally, I think cloud is another important way by which we can start working together.”

In its attempts to become a content provider, Google has prioritized YouTube — mentions of YouTube now outpace those of Google’s largest business, Google Search, on company earnings calls.

In addition to new streams of ad and subscription revenue, innovation in content also stand to benefit Google’s cloud business, as faster streaming capacity and reduced latency will require higher levels of computing power. Notably, music streaming service Spotify and video streaming service Netflix have moved away from AWS and Azure in favor of Google Cloud Platform (GCP) services.

WHY this initiative?

When it comes to digital commerce, Google’s main objective is to protect its advertising business from all angles. Product search is a critical component of Google’s business, and the company cannot afford to lose more of that business to e-commerce giant Amazon.

On the content side, Google’s ability to engage with consumers in gaming and media streaming could present another avenue to deploy its advertising business, as well as an additional source of data collection to improve its search and advertising capabilities.

5. Expand in India & Southeast Asia, rebuild presence in China

A number of Google’s recent investments, partnerships, and internal projects suggest an interest in building out a presence in India and Southeast Asia, two regions that are experiencing outsized growth in internet usage.

Google’s recent activity also suggests that China is on its radar, despite historical tension between the tech giant and the Chinese government.

These emerging economies offer incremental revenue streams as connectivity improves and more and more consumers gain access to the internet.

WHAT IT’S DOING now

Google has ramped up its investment in emerging markets in recent quarters, namely in India and Indonesia — two countries seeing explosive growth in digital commerce.

Building up its e-commerce presence allows Google to capitalize on the growth in these regions while also maintaining its foothold in search and advertising.

Investments

In January, Google participated in a $1.5B tranche of Series C funding to Indonesian ride-hailing giant GO-JEK. Similar to Uber, GO-JEK also offers food delivery services and a mobile payments platform.

The GO-JEK investment was Google’s first investment in Indonesia. The deal came less than a month after Google made its first investment in India, contributing to personal concierge and delivery service platform Dunzo’s $12M Series B round in December.

In addition to India and Southeast Asia, Google has set its eyes on China, despite historical setbacks in the country.

While many view China as a missed opportunity for Google, the company has stepped up its investments in the region. Recent investments include a $550M investment in JD.com, China’s second-largest e-commerce platform, and a $76M investment in China-based gaming firm Chushou.

Google’s return-focused investment arm capitalG has also made a number of investments to companies based in India and China.

According to Kaushik Anand, the head of capitalG’s operations in India, capitalG looks to back “sustainable business models operating in large markets.” India serves as a substantial opportunity on that front, given that the country has the second largest internet market in the world after China, with over 450M uers.

CapitalG’s recent deals abroad include investments in India-based fintech company Aye Finance’s $21.5M Series C in June – the fund’s first fintech investment in India – as well as in Chinese truck-hailing platform Manbang Group’s $1.9B round in April.

Google has also dedicated internal resources to connecting remote parts of the globe. Loon, Google’s moonshot project for remote telecommunication projects, recently graduated from X to became its own company under the Alphabet umbrella. Loon can launch balloons 12+ miles into the stratosphere to provide cellular coverage in remote areas or areas affected by natural disasters. In July, Loon announced that it will launch its first commercial service in Kenya next year, offering 4G coverage via its high-altitude balloons.

Product launches

Google launched mobile payments platform Tez in India in September 2017. Tez is a free mobile wallet that allows users to make payments directly from their bank account. Through Tez, Google is ultimately attempting to become an integral part of commerce in India, which offers a huge opportunity for growth.

WHERE IT’S GOING next

Google has only just begun its foray into India & Southeast Asia and its re-entry into China, but expansion in these markets seems to be crucial to its strategy moving forward.

News

Google’s partnership with JD.com will likely give it an opening to re-establish itself in China, given that JD is the second-largest e-commerce player in China (after Alibaba) and has a notable hold on the consumer space in the country.

More broadly, the JD.com partnership could offer Google the opportunity to strengthen its hold on product searches and voice-driven e-commerce, even as competitors such as Amazon chip away at its foothold.

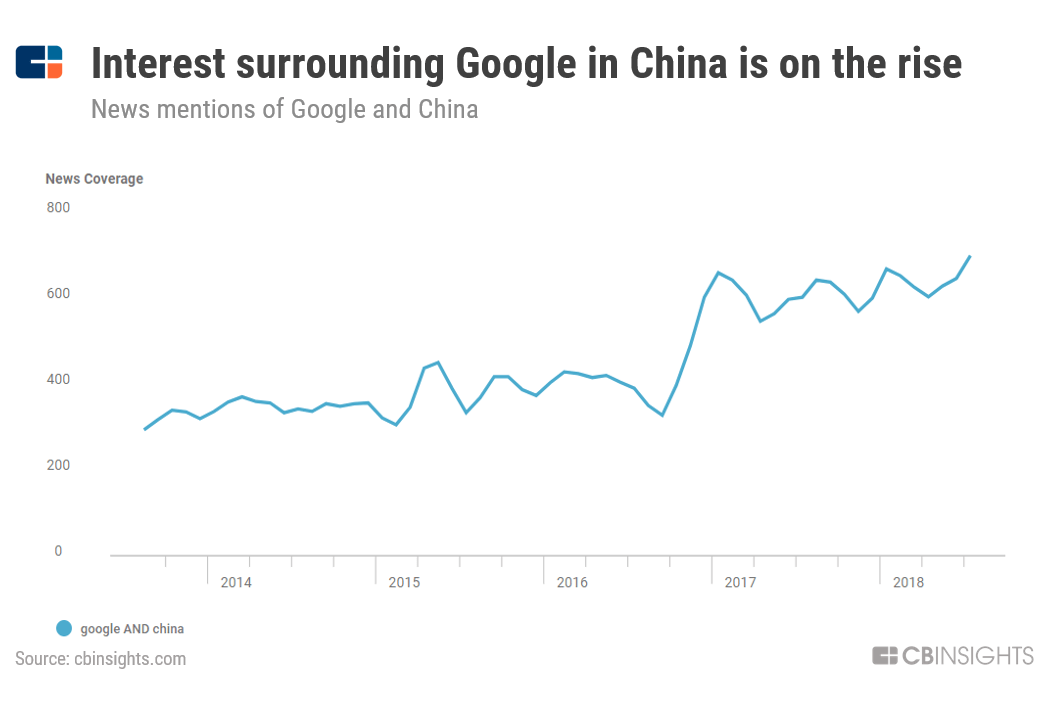

Google has also made headlines in recent weeks amid rumors that it has been tracking search queries to develop a censored search engine in China. Google has historically had tense relationships with governments and consumers in China, withdrawing its desktop search engine from the country roughly 8 years ago following a phishing scandal.

Despite these tensions, China presents a unique opportunity for the firm: the company’s internet market has grown substantially since Google pulled its search platform, and the majority of its 770M+ internet users are accessing the web through Google’s Android operating system.

Google is also looking to take advantage of China’s growing cloud market and is seeking to offer its cloud services out of data centers run by local companies, according to recent reports.

Earnings transcripts

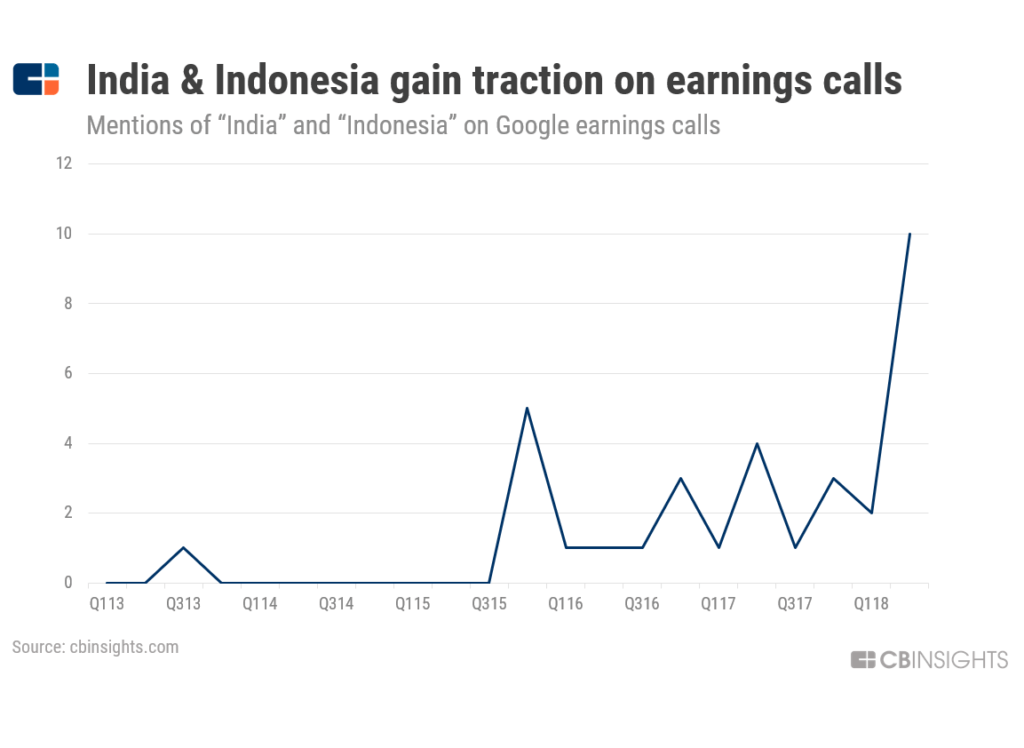

India and Indonesia came into focus on the company’s Q2’18 earnings call, given the company’s recent investments.

CEO Pichai outlined the importance of these regions in more detail on the call:

“I want to highlight the work that we’re doing to build great specialized products for the next wave of people coming online for the first time in countries like India, Indonesia, Brazil, and Nigeria, many of whom experience the web only through their mobile phone. This is a big area of focus for us.”

WHY IS THIS A PRIORITY?

As internet access improves globally, a number of emerging markets are seeing outsized growth in internet usage and growing demand for connected devices. Southeast Asia, for example, reportedly has rising internet adoption across more than 600M consumers.

This presents a substantial opportunity for Google’s expansion.

CEO Pichai has cited emerging markets as a notable avenue for growth:

“The user growth there is extraordinary. And we are seeing it across all our products, which have over a billion users each and we are all doing well in these markets.”

Market sizings

The revenue opportunity in these spaces is substantial. According to consensus analyst estimates, the e-commerce markets in India and Southeast Asia are expected to reach roughly $200B and $88B by 2025, respectively.

Alongside growth in digital commerce is an opportunity in payments. In India, the payments industry is expected to reach $1T by 2025, and in Southeast Asia, analysts estimate the market could reach $200B. Establishing a presence in these more nascent markets could pay off for Google, and capturing even just a segment of these markets could serve as a notable revenue opportunity.

6. Disrupt the transportation and logistics industry

Alphabet has placed a number of strategic bets in the transportation space across its investment arms, and its several ongoing internal projects suggest the company is seeking to capitalize on the future of transportation.